By Nitya Jaisinghani and Margaux Koegler

Introduction

In the fast-evolving world of finance, new investment strategies and vehicles continue to emerge, reshaping the way investors manage their portfolios. One such innovation that has garnered increasing attention in recent years is the semi-liquid fund. A financial instrument that bridges the gap between traditional open-end mutual funds and less liquid closed-end investment options. In this article, we will delve into the rise of semi-liquid funds and their profound impact on modern portfolio management.

Understanding Semi-Liquid Funds: a Middle Ground for Diversification

A. Definition and Characteristics

A semi-liquid fund, also known as an interval fund, is a distinctive investment vehicle designed to provide a balance between the liquidity and illiquidity of assets within a portfolio. Unlike traditional open-end mutual funds, semi-liquid funds operate with predefined redemption intervals, typically occurring on a quarterly basis. This unique structure allows investors to request redemptions only during these specific timeframes, introducing a level of flexibility while still retaining some of the characteristics associated with less-liquid investments.

Semi-liquid fund investors can withdraw their capital at least quarterly, or sometimes even monthly. However, the investment vehicles require a predetermined limit as to how much investors can withdraw. They set redemption limits that ensure managers do not sell assets for a lower return in a panic.

B. Evolution of Investment Vehicles

These innovative investment vehicles, offering a middle ground between traditional open-end funds and less liquid options, have gained momentum over the past two decades.

Among the early adopters, dating back to the early 2000s, we find pioneers like Partners Group. They’ve ventured into the realm of semi-liquid funds, offering opportunities in private equity, real estate, and private debt. However, since 2018 the trend has truly accelerated. Not only have established players in the French market—such as Eurazeo, Apax, and Ardian—embraced it, but renowned global giants such as Blackstone, Hamilton Lane, Sequoia, Schroders, and StepStone have also jumped on board, augmenting their offerings with at least one evergreen fund.

There are two vehicles which are specialised in semi-liquid structures: Business Development Companies (BDCs) and Real Estate Investment Trusts (REITS). These two vehicles have interval repurchase provisions (funds periodically offer to buy back a percentage of outstanding shares at net asset value) to which managers know investors are attracted to. They are not unlike interval funds as they have liquidity provisions(guarantee that buy and sell prices do not become too volatile) and are registered with the SEC. Many large PE firms such as Blackstone, Starwood, Apollo, and others have explored the semi-liquid space in recent years, such as Blackstone’s Real Estate Income Trust, which will be explained more.

There are multiple benefits to semi-liquid evergreen (open-ended) funds compared to traditional funds aside from the liquidity aspect. They provide to their investors an income source that is stable and received at intervals, as well as immediate private markets exposure. Another advantage is the autonomy of the investor to choose how long of an investment period they would like to choose and they receive compounded performance over time.

The traditional drawdown fund would require capital investments (capital calls) over the course of a few years whereas semi liquids require a full contribution commitment at the start. Semi liquids also have a feature known as liquidity sleeves – where investors’ capital is held in the form of public market investments and/or cash if it could not be immediately matched with a private investment option.

Capitalising on Opportunities: the Benefits of Semi-Liquid Funds

A. Enhanced Portfolio Diversification

Semi-liquid funds distinguish themselves by offering investors exposure to a wide array of alternative assets that may not be readily accessible through traditional investment avenues. These assets span a varied spectrum, including private equity, venture capital, real estate, and other non-traditional investments. By incorporating such alternatives, investors can mitigate risk and potentially enhance returns by tapping into markets and opportunities that conventional investments often overlook

By spreading investments across different asset classes, industries, and geographic regions, investors can reduce the overall risk of their portfolios.

In the context of semi-liquid funds, the ability to include alternative assets in a portfolio adds a layer of diversification that goes beyond traditional stocks and bonds. Alternative assets often exhibit lower correlation with mainstream markets, meaning their performance may not be closely tied to the movements of more conventional investments. This lack of correlation can act as a stabilising force, helping to buffer against the volatility that may affect traditional assets during economic downturns.

Moreover, the inclusion of alternative assets in a diversified portfolio may offer the potential for enhanced returns. Private equity investments, for example, may generate alpha by capitalising on opportunities that arise in less efficient markets, contributing to overall portfolio performance.

B. Illiquidity Management and Consistency exposure to private markets

One of the main challenges posed by traditional illiquid investments is the long lock-up period, which can extend over several years. These funds require investors to commit their capital for an extended duration, which can range from five to ten years. During this time, investors generally do not have the option to access their investments until the fund manager initiates capital calls for new investments or distributes returns from realised investments. Since traditional closed-end funds are relatively inflexible, it is difficult for investors to access their funds in the event of unforeseen financial needs or a change in investment strategy.

Semi-liquid funds provide a solution to this challenge by establishing predefined redemption intervals, often occurring quarterly. Indeed, investors can request redemptions at specified times during the year. Therefore, this structure allows investors to maintain some liquidity while still having exposure to less-liquid asset classes. The fact that investors can access their investments at these intervals offers greater flexibility. This allows investors to make adjustments to their portfolios and respond to financial needs more readily.

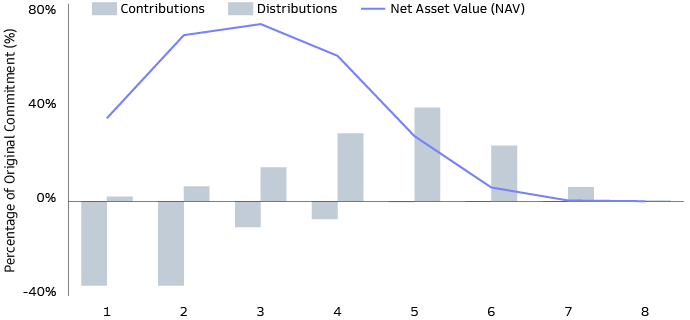

Regarding private market exposure, in traditional funds, the net asset value of investors typically follows a bell curve which rises from the early years (when the fund’s investments are made) and then tapers off in later years (as investments are harvested). On average, the fund’s net asset value reaches its highest point at 70-80% during the initial commitment of the investors. Therefore, investors ought to enhance their exposure to private markets.

Managers of traditional drawdown funds can benefit from knowledge of the total capital available to deploy over the full investment period, making it easier to establish diversification (e.g., position sizing) parameters. Investors’ exposure to private markets follows a ‘bell curve’, which ramps up during the early years of the fund as investments are made, and winds down in later years as investments are harvested. On average, the fund’s net asset value peaks at 70-80% of the investor’s initial commitment. Investors should optimize their private markets exposure via a steady commitment program to new funds each vintage year.

C. Access to expertise and reduced volatility

Investors who usually invest in private markets are not as subject to short term volatility since they are aware that they have to play the long-term game to see any major profits. However, in semi-liquids, many of the investors are not as experienced or knowledgeable. Therefore, it is the role of the manager to supply outsized returns to LPs, as well as diversify risk so the LPs do not panic during downtimes.

Furthermore, semi-liquids are designed for investors who are attracted to private market investment upsides, which are generally reserved for long-term illiquid investments, while giving them liquidity benefits. This is done to draw in investors who are part of the mass affluent, but who may not have a well established liquidity situation under control. Accredited investors would probably allocate a percentage of their portfolio to private markets for the high returns, but also would allocate a generous portion to other asset classes to meet their liquidity requirements.

Evergreen vehicles have the benefit, due to their liquid nature, that other non-liquid vehicles do not have. For example large scale transactions will not affect the market as much due to evergreen vehicle’s liquidity which ensures smooth performance. However, the downside of the liquidity feature is that during periods of higher economic stress, liquidity is depleted.

Challenges and Considerations: Navigating Semi-Liquid Funds Investments

A. Limited Redemption Opportunities

An example is BREIT, Blackstone’s REIT which follows the semi-liquid fund structure created for individual investors. It was an opportunity for retail investors to get involved in the Commercial Real Estate market for as little as $2,500. The semi liquid facet was that investors could sell back their shares every month to BREIT, if they chose to leave. BREIT had strong returns of 11.3% as compared to the Cambridge Associates PE Index 5 year return of 17.77%. Then, a crisis. The stock market took a downturn, interest rates rose sharply, and the property market plunged. Many BREIT investors consisted of small investors, who were prone to making intuitive decisions and retracted their shares almost immediately, as well as Asian investors who when faced with market decline sold their BREIT shares as it was one of the few well performing funds. Blackstone was accustomed to experienced and methodical long term investors which is who they primarily deal with.

BREIT received so many requests to sell from their investors that the fund could not liquidise enough at that rate. The fund then enforced a provision which limited withdrawals that investors could make. This led to a plummet in stock prices, almost 20% decrease in one month.

B. Fees

The performance fees in this asset class, part of the private market, are usually a percentage of the excess return. It could be around 15-20% of the return, which aligns the interest of the manager of the investment as well as the investor. The manager will be incentivised to yield higher excess returns for the investor so they can both profit.

Semi-liquids must have a liquid component to provide their semi liquid promise. That means that about ¾ of the fund is invested in private equity. However, the remainder ¼ of the fund is kept in the liquid sector – money markets. This means that since ¼ of the fund is not invested in private equity then there is no way it can return private equity level returns.

Conclusion: Semi-Liquid Funds as a Modern Portfolio Management Solutions

Semi-liquids provide access to private markets for HNWIs. It is considered a solution for balancing private market returns with the liquidity of money market investments. There are a few things to watch out for, however, including that during times of economic duress, the investors are not experienced and may panic. Due to this, semi liquids may have limits on withdrawals so as to protect investors as well as the nature of the fund. However, semi-liquids are still more flexible than traditional funds and offer investors an opportunity to invest while retaining a reliable source of income.

Sources

https://www.privateequityinternational.com/why-semi-liquids-are-not-just-for-wealthy-individuals/

https://www.privateequityinternational.com/semi-liquids-mapping-the-universe-of-pe-wealth-products/

https://www.wsj.com/articles/blackstones-big-new-idea-leaves-it-bruised-d66de361

https://www.cambridgeassociates.com/wp-content/uploads/2023/10/WEB-2023-Q2-USPE-Benchmark-Book.pdf

Comments are closed.