Martina Pertusi, Raffaele Lanteri, and Manfredas Feiferas

Introduction

First developed in 1983 by Irving Grousbeck, a search fund is an investment vehicle through which investors support an entrepreneur’s efforts to find, acquire, and take over the management of a company to make it grow. In the early 90s, this model was exported to the UK – marking the first instance of a search fund outside the US; since then, the model has spread like wildfire throughout Europe. This article will discuss the intricacies and uniqueness of the search fund model, to determine its feasibility in the Italian Private Equity market.

Phase 1: Structuring and Raising Capital

The initial phase of search fund operations involves structuring the search fund and raising the initial capital. Once committed to the search fund, the search capital obtained is used to establish the fund and cover the salaries and administrative expenses needed to finance the research of the target company. The searcher reaches out to a broad network of potential investors, including friends, family, angel investors, business schools, associates, business owners, executives, institutional search fund investors, or crowdfunding platforms.

The search for investors is a strategic process, as these individuals not only contribute financially, but also become future advisors offering guidance, expertise, and networking opportunities.

The fundraising process begins with a formal Private Placement Memorandum (PPM) created by the principal, outlining the investment opportunity. The PPM covers various aspects, including the executive summary, search fund model overview, methodology, industries and geographic scope, screening criteria, activity timeline, budget, investment structure, return on investment, exit strategy, and the principal’s background and motivations.

Investors receive the PPM, leading to meetings to evaluate alignment in terms of goals, industry focus, geography, and others. Once an investor believes in the fund proposition, they transfer the money in exchange for a share or shares of the fund. Capital providers gain the right to be informed when a target is identified and have the right of first refusal on acquisition capital. This allows them to decide whether to participate in the acquisition capital, obtain an equity stake in the target, or decline and receive a share of 1.5 times the search capital invested. Maintaining relationships with investors, whether they participated in the search or not, is crucial, as some may prefer to commit to a known target rather than fund a search.

Phase 2: Sourcing the Target

Next, the principal, having successfully raised the necessary funds, embarks on the challenging task of identifying a suitable acquisition target. This phase is time-consuming, averaging around 19 months, during which the searcher defines industries of interest based on criteria such as fragmentation, growth records, and product lifecycle. They then employ both quantitative and qualitative variables to narrow down potential targets, considering financial aspects as well as personal preferences and the willingness of the business owner to sell.

Two main approaches to sourcing firms emerge: the broker deal flow – involving third-party referrals from professional institutions – and the proprietary approach – where the searcher independently seeks potential targets. The former relies on specialised brokers and offers advantages in overcoming owner reluctance to sell, although it may result in more competition and higher costs. The proprietary approach demands significant effort, with the searcher directly contacting business owners, utilising various channels, and leveraging personal and professional networks. Many searchers adopt a hybrid strategy, using both approaches to maximise opportunities. Involving the investor base becomes crucial, as experienced investors provide insights, niche focus, and direct introductions to target owners.

Phase 3: Evaluating and Founding the Transaction

After compiling a shortlist, a search fund enters the third stage (also known as The Closing): evaluating potential targets and determining the optimal capital structure. This phase involves securing acquisition capital from stakeholders. The evaluation, lasting 6 to 12 months, includes preliminary due diligence, business valuation leading to a Letter of Intent, and comprehensive due diligence leading to closing. The goal is to finalise the deal, requiring the searcher to identify the right target, sign a Letter of Intent, conduct meaningful due diligence, agree on terms, and secure equity and debt financing. Success demands strategic resource use, prioritisation, and disciplined attention to detail, while maintaining a strong relationship with the seller and avoiding tunnel vision.

Phase 4: Transition Period and Value Creation

Following the acquisition, the searcher assumes the role of the new CEO, bringing forth a set of crucial tasks. Initially, communication plays a pivotal role as the new CEO officially announces the change in ownership to employees, suppliers, customers, and other key stakeholders. Simultaneously, a transition period is introduced, if agreed upon with the seller, allowing the former owner to remain in the company for a fixed duration to facilitate a smooth handover.

The transition period, ranging from 6 to 18 months, involves the seller’s continued involvement in the company, aiding the new CEO’s understanding of business routines and alleviating uncertainties among employees and stakeholders. Moving beyond the transition period, the CEO collaborates with management to execute growth plans developed during the earlier phases. These growth strategies encompass both organic and inorganic approaches, tailored to the specific needs and opportunities of the company.

Phase 5: The Exit

Lastly, the searcher develops an exit strategy and the realisation of value created through a well-executed strategic growth plan. A search fund seeks to buy and sell a business after a holding period, aiming for a higher return compared to other asset classes to compensate for the opportunity cost of capital and the risks associated with the investment.

The holding period for a search fund is typically longer than that of a normal private equity fund, lasting around 7 years. This extended period allows the searcher to understand the business, demonstrate commitment to long-term value, and align with investors’ willingness for a prolonged investment. Exit strategies for a search fund include selling or merging the business with a strategic or financial buyer, going public through an Initial Public Offering (IPO), share buyback, share purchase by new or current stockholders, and debt restructuring with a dividend pay-out. Naturally, the size of the target business can affect the feasibility of certain exit strategies. Furthermore, the timing and method of exit depend on investor needs and decisions made by the CEO and board of directors.

Facts and Figures

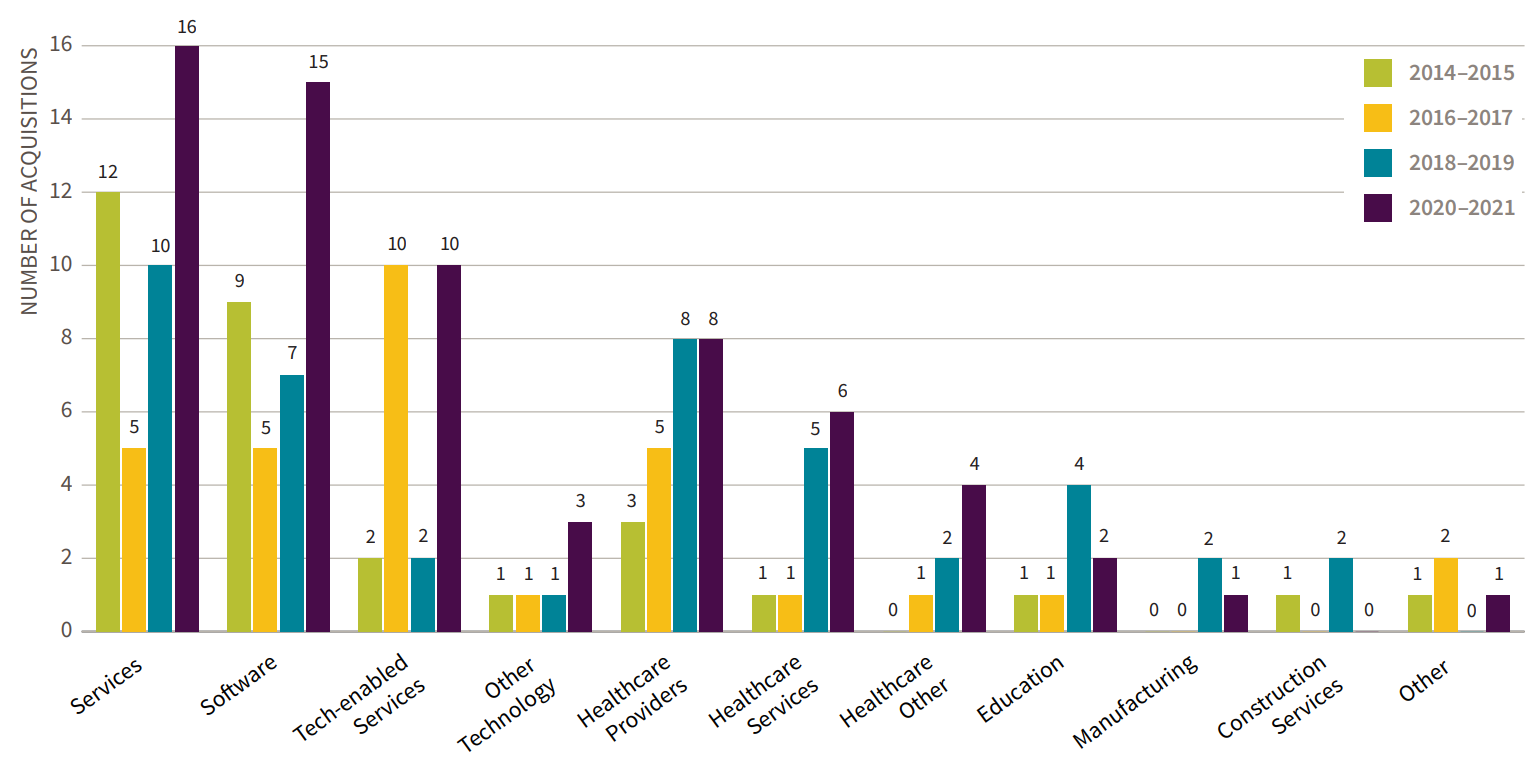

The figure below displays how the acquisitions by search funds are spread across different industries. As it can be seen services, software, and healthcare – have been the hottest industries for search funds to invest in. As seen from the graph below, the greatest growth in the volume of acquisitions from 2014 to 2021 can be seen in tech-enabled services and software. As the latest considered acquisitions occurred during the Covid-19 pandemic it is crucial to note that growth in services, software, and tech-enabled services were the greatest volume underpinning the importance of being reactive to the macroeconomic climate. Furthermore, even though the search funds invest in a variety of industries they have a common ground: strong growth, strong margins, and recurring revenues.

Industries of Acquired Companies (Kolarova, 2022)

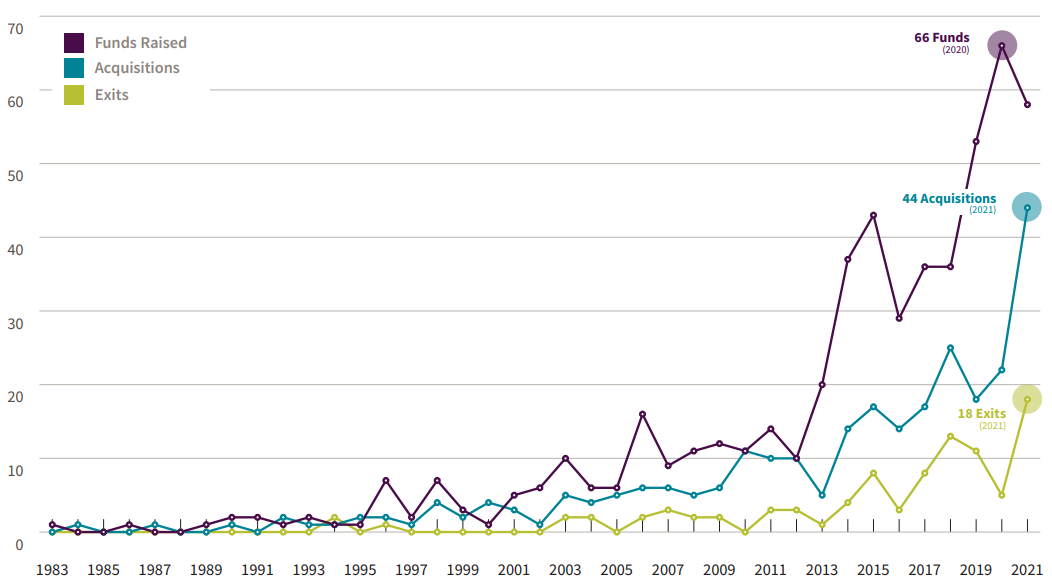

When looking at the timeline of the establishment of various search funds, it can be said that the activity of search funds before the 2000s was not as significant, leading to few raisins, acquisitions, and exits in the industry. Fundraising for the search funds has especially spurred during the periods from 2011 to 2015 and between 2017 and 2020. Granted, acquisitions and exits by search funds follow, but they are delayed, as it takes time to search for a company and after a while to exit it. In recent years, the most noticeable disparity between fundraising and investment can be seen in 2021.

Search Fund Activity by Year (Kolarova, 2022)

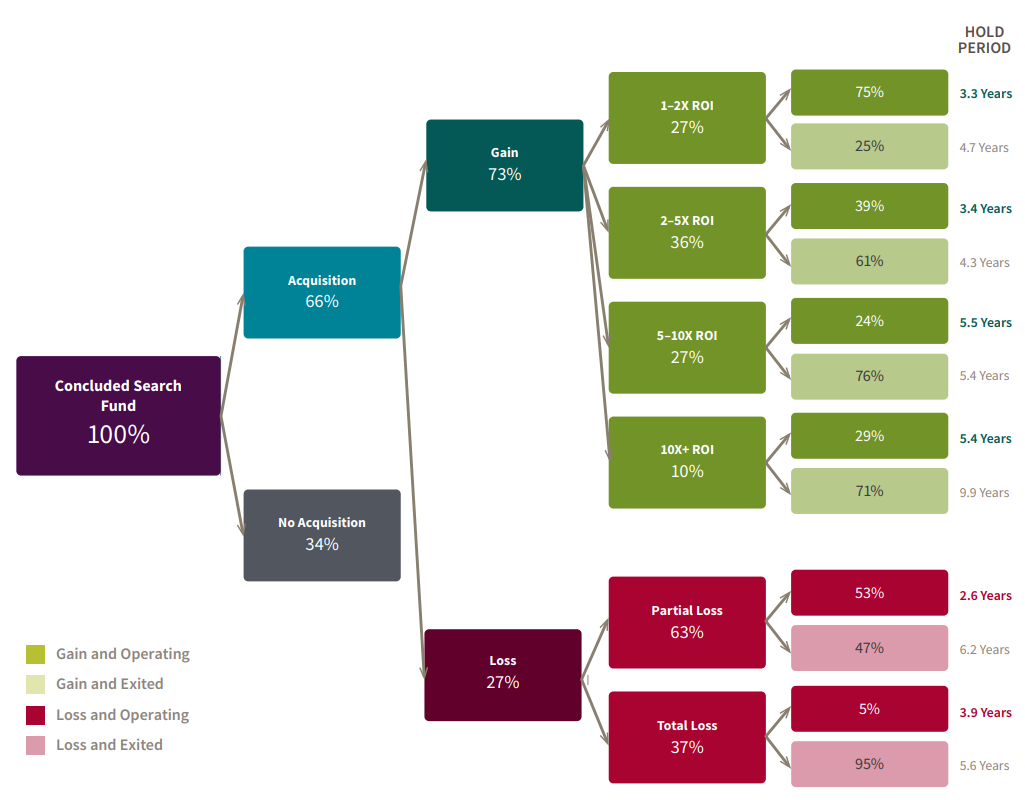

Lastly, it is interesting to note how successful the search funds are – displaying 66% of search funds leading to an acquisition, while if the investment occurred then in 73% of the cases it led to a gain, while there was a 27% of loss, of which 63% was a partial loss, while 37% leading to a total loss. It is important to note that for loss to happen it can take anywhere from 2.6 years to 5.6 years. Nonetheless, most cases display that there has been a gain created by the search fund. Return on investment (ROI) for different search funds varies from 1x to 10x or even more. Notably, an ROI of 1-2x can be found in 27% of gain-generating funds, 2-5x ROI is found in 36% of gain-generating funds, and 27% – experienced an ROI of 5-10x, while only a small minority of 10% of the funds reached the ROI of 10x+, which in turn tends to lead to a higher holding period for the fund. As seen in the graph below, the period of hold varies from the smallest being 3.3 years to 9.9 years.

Search Fund Outcomes (Kolarova, 2022)

Feasibility of Search Funds in the Italian Market

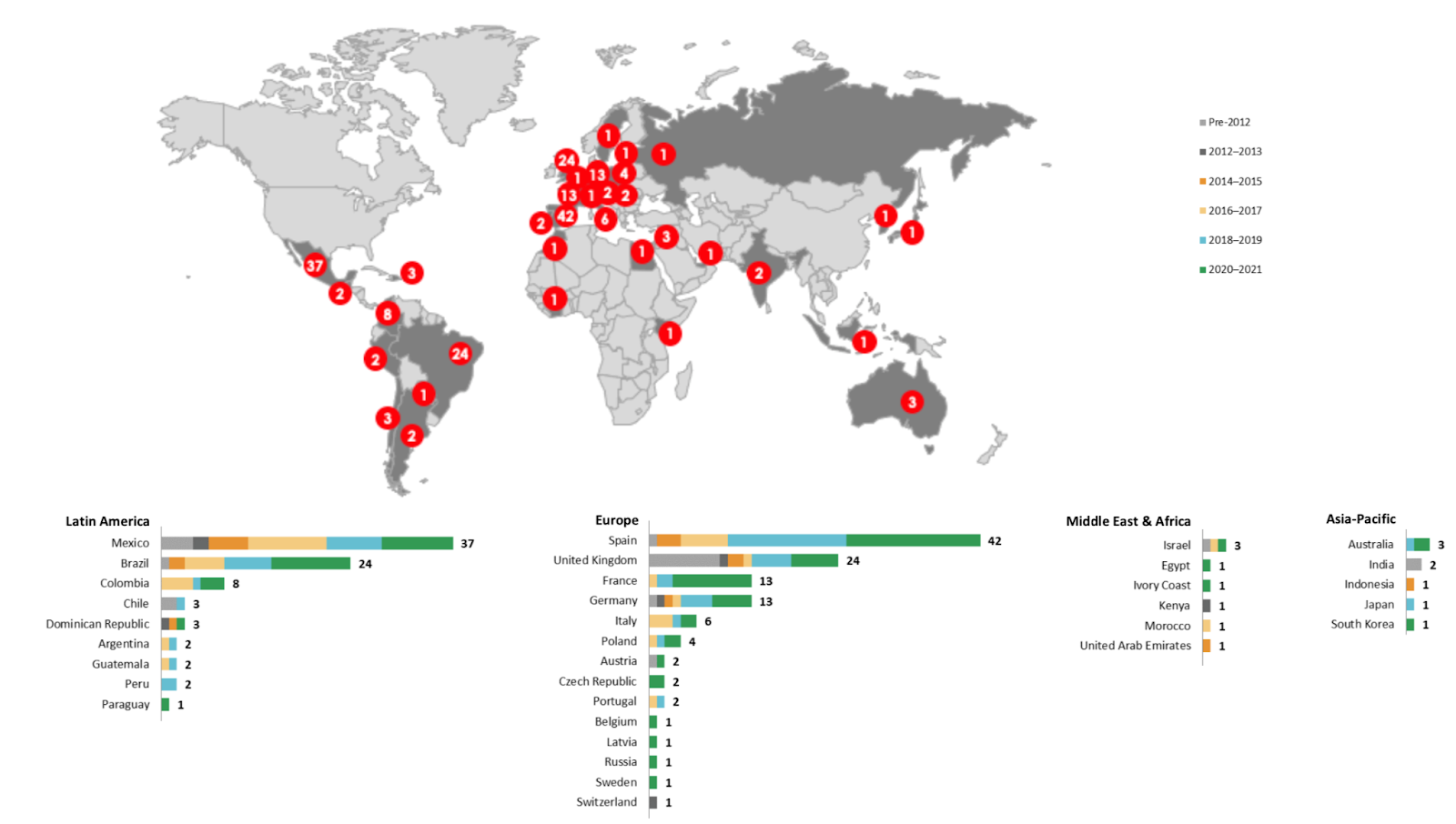

Most searchers were MBA graduates returning to their home countries after attending the most prestigious universities, and disproportionately US-based – where the model was continuously taught within entrepreneurship classes. According to some studies, there is a positive correlation between the engagement of institutions like universities and the number of searchers that embrace this path.

International Search Funds by Country (Kolarova, 2022)

The search fund model arrived in Italy in 2016 thanks to some Italian MBA graduates coming back from their experiences abroad. Due to the above-mentioned characteristics of the model, search funds are particularly interesting for the Italian market. The latter is characterised by a high number of family-owned SMEs and many face a delicate situation at the time of generational transition. According to the Family Firm Institute, family businesses constitute roughly 2/3 of the world’s enterprises, while in Italy they account for 85% of the active companies.

Moreover, as highlighted by a Deloitte Report, it is also crucial to take into consideration the demographics behind the leaders of these companies: 23% of Italian family businesses are led by a person who is more than 70 years of age. Generational continuity is one of the most critical matters that family business has to encounter; based on AUB-ISTAT data, 18% of companies should change their leaders in the next 5 years, while only 9% of them take it into real consideration. It is precisely in this context that the search fund model finds a fantastic opportunity in Italy, targeting those deals that are too small for institutional investors and too big for most business angels.

Sources

https://www.iese.edu/media/research/pdfs/OP-0630-E

https://polsky.uchicago.edu/wp-content/uploads/2018/03/Booth-Research-Evolution-of-ETA_FA110716.pdf

https://thesis.unipd.it/retrieve/261179e3-7f62-4bdb-a315-8f13d5d93378/Scarato_Michele.pdf

https://www2.deloitte.com/content/dam/Deloitte/it/Documents/strategy/Il%20passaggio%20generazionale%20e%20il%20family%20business_deloitte%20italia.pdf

https://www.gsb.stanford.edu/experience/about/centers-institutes/ces/research/search-funds

https://www.searchfund.it/descrizione/search-fund-mercato-italiano

Comments are closed.