By Benedetta Visconti, Elias Emery, and Annacarla Bianco

Introduction

Private equity firm Silver Lake recently announced that it was working on a proposal to take talent and media company Endeavor Group Holdings private after Endeavor announced it had begun a review to explore alternatives that better value the company. Endeavor stated it was evaluating strategic options but would not consider a sale or disposition of its majority interest in TKO Group Holdings, which includes a stake in Ultimate Fighting Championship, a major source of revenue and advertising. Silver Lake, which holds about 71% of the voting power of Endeavor, issued a statement saying it was not interested in selling its shares to a third party or entertaining bids for assets that are part of the media group. Endeavor Group, which has diversified holdings in talent management, live sports, and festivals, is valued at around $11.5bn as of 29 November, 2023.

Silver Lake Management

Silver Lake is an American private equity firm focused on investments in technology, technology-enabled, and related industries. Founded in 1999, Silver Lake has since become the 11th-largest private equity firm in the world in terms of its assets under management. The firm was promising in even its earliest days because its founders had decades of entertainment and technology focused deals among them. Jim Davidson had led the Technology Investment Banking business at Hambrecht & Quist., David Roux had an operational and entrepreneurial background, having served as chairman and CEO of Liberate Technologies, a software development firm. Roger McNamee was formerly an investment representative of Integral Capital Partners. Lastly, Glenn Hutchins, who came from Blackstone, had served as a Special Advisor on economic and healthcare policy in the early Clinton Administration. To sum things up, Silver Lake was not only formed by leaders in the private equity industry, but also by people who had experienced billions of dollars worth of transactions in the exact area Silver Lake was to focus on.

Davidson, Roux, McNamee, and Hutchins all agreed that they would take advantage of the recent technology boom of the late 1990s to make private equity investments in mature technology companies, as opposed to the startups that were generally pursued actively by venture capitalists. Since its inception, Silver Lake’s portfolio companies have consisted of the likes of Airbnb, Alibaba Group, Ancestry.com, Karma, Dell Technologies, Fanatics, GoDaddy, Qualtrics, Skype, and Twitter, among many others. Such investments have contributed to Silver Lake’s massive and rapid growth to $98bn assets under management since inception, with an average IRR of 17.1% on all of its investments, which it typically hold for 5 to 7 years.

Today, Silver Lake splits up its technological focus into several different verticals: Compute & Communications, Enterprise Software, Financial Technology, Health & Learning, HR Services, Internet & eCommerce, IT Management Software, Mobility, Real Estate Technology, Security, and Software Application Development. All the previously mentioned sectors generally consist of either a hardware or software component, but are generally grouped together under the phrase “technology.” Despite being the global leader in technology-focused alternative investments, Silver Lake has an additional, more consumer and personal-focused division: Content & Entertainment. This group has been just as successful as its counterparts with holdings of Australian Professional Leagues, City Football Group, and Madison Square Garden Sports, but it all started in 2012 with a minority stake in what was then known as William Morris Endeavor.

The History of Endeavor’s Ownership

The Endeavor Talent Agency was launched in 1995, and it became one of the fastest-growing Hollywood talent agencies by 2009. It shortly became William Morris Endeavor, or “WME,” after merging with William Morris Agency on April 27th of that year. Endeavor executives Ari Emanuel and Patrick Whitesell were the architects of the merger and quickly became the Co-CEOs of WME. Emanuel and Whitesell were eager for Endeavor to grow to include several subsidiary companies and expanded divisions. Shortly after the merger, WME helped launch the investment group Raine, which aligned the company with properties like Vice Media and Zumba Fitness. Additionally, WME partnered with RED Interactive, a digital advertising agency in 2010. Two years later, they allied with the social media management firm TheAudience, where they partnered with digital entrepreneurs and executed social campaigns for major motion pictures. The visible dominance of WME caught the attention of many investors, who wanted the opportunity to capitalize on its rapid growth to $9bn in an industry worth $20bn.

On May 2, 2012, WME and Silver Lake Partners, signed an agreement for Silver Lake to acquire a 31.25% minority stake in the agency for $250mn. A new executive committee, consisting of WME’s Co-CEOs and Silver Lake Managing Director Egon Durban worked together to form a new executive committee, which would take the lead on the company’s growth strategy and investment activities. Shortly after the deal in July 2013, WME acquired a minority stake in the creative agency Droga5, which would combine the companies’ advertising and entertainment resources. This was the start of WME’s dominance in the entertainment industry. In December of that year, WME and Silver Lake announced the acquisition of IMG for $2.4bn, which would lead to the creation of WME-IMG. In 2015, WME underwent a spurt of acquisitions consisting of Global eSports Management in January, Professional Bull Riders in April, and the Miss Universe Organization in September. The most impactful purchase, however, occurred in July of 2016, when Silver Lake helped back WME-IMG’s acquisition of the UFC. The UFC brought record revenues from advertising, merchandise, and pay-per-views, and ultimately led to the formation of a new holding company, Endeavor, which took on the full portfolio of owned and operated brands formerly under the WME-IMG banner.

With Silver Lake’s financial advisory, Endeavor had quickly grown to become one of the largest entertainment conglomerates in history and would thus be well suited to being on the public market, as many investors had contributed to its raising capital. On May 24 of 2019, Endeavor filed forms for an IPO with the SEC that have valued the company at $7.6bn. At the time, Endeavor’s revenue was $3.61bn with a net income of $100.1mn after adjustments. Since its IPO, Endeavor Group Holdings Inc. has traded on the New York Stock Exchange under the ticker EDR. Its growth and industrial expansion have since continued, but in October of this year, Silver Lake announced plans to increase its 71% stake in the entertainment giant and make it entirely private.

Industry Overview – A League of Its Own

Ever since Endeavor acquired TKO Holdings during the summer of 2023, it has become the clear market leader when it comes to combat sports, owning $12.1bn of around a $17bn industry It has the luxury of owning the parent company of both the WWE and the UFC, which are both industry leaders in their respective sports. Rival companies such as the AEW and ONE Championship are nowhere near competitive in market value, viewer rates, and levels of competition. Therefore, when it comes to combat sports entertainment, there is no reason to believe that Endeavor will not remain at the top. Endeavor’s subsidiaries have performed so well that it is even being compared to streaming giants Paramount Global, Live Nation Entertainment, and Fox Corporation in terms of enterprise value and overall sales. Regardless of Endeavor not fitting into a specific sector, Silver Lake would be happy to have the market leader in fighting all to itself.

Deal Rationale

Silver Lake’s proposal to privatize Endeavor Group Holdings is primarily motivated by the belief that the company is undervalued in the public market, leading to a focus on maximizing shareholder value. With Endeavor’s market capitalization at approximately $11.46 billion, CEO Ari Emanuel has pointed out that Wall Street’s valuation does not reflect the company’s true worth. This discrepancy between the public market value and the alleged intrinsic value of Endeavor’s assets has pushed the company to engage in a strategy to realign the market valuation with its actual value. This privatization aims not only to provide a more accurate valuation but also to provide higher financial flexibility, enabling more effective implementation of long-term strategies without the constraints of public market pressures. Additionally, Silver Lake, holding significant shares in Endeavor, is not looking to sell to third parties or entertain offers for media group assets but to align with Endeavor’s own review to explore strategic alternatives that better recognize the company’s value.

Hence, Silver Lake’s privatization proposal for Endeavor suggests a strategy aimed at unlocking value. While specific initiatives by Silver Lake haven’t been disclosed, such private equity strategies typically involve operational efficiency improvements, strategic redirection towards high-margin areas, and financial restructuring. Silver Lake could potentially consolidate Endeavor’s position through selective acquisitions, divest non-core assets, and tap into digital transformation opportunities. These speculative measures could streamline operations, reduce costs, and diversify revenue streams, creating a more robust platform poised for growth beyond the immediate visibility of public markets.

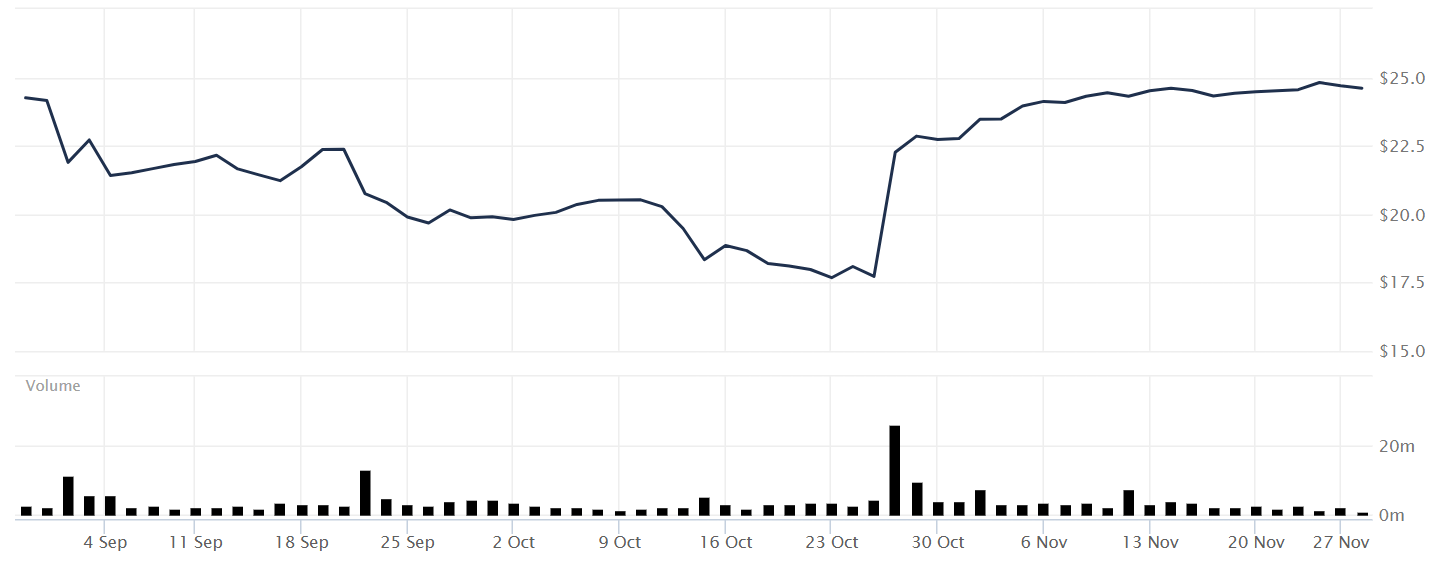

On October 25, 2023, the day Silver Lake announced its privatization proposal for Endeavor, the company’s stock opened at $17.86 and closed at $17.72. By October 27, the stock opened at a notably higher $22.19 and closed at $22.85, marking a significant 29% increase from the announcement day’s closing price, as shown in Exhibit 1. This sharp rise in Endeavor’s share price reflects robust investor confidence in the potential advantages of privatization. Indeed, market reactions like this typically indicate expectations of more efficient operations, improved strategic focus, and an increase in the company’s perceived intrinsic value post-privatization. The substantial increase in the share price implies that investors anticipate the privatization will reveal and enhance Endeavor’s value beyond its current public market assessment.

Exhibit 1

The move to privatize Endeavor gains significance against the backdrop of significant industry transactions, like French billionaire Francois-Henri Pinault’s acquisition of a majority stake in Creative Artists Agency, valued at $7 billion. Such deals exemplify a broader industry trend of strategic consolidations, diversification, and acquiring competitive advantages. This broader context illuminates Silver Lake’s decision for Endeavor, highlighting a common strategy among companies across various sectors to reevaluate and optimize their approaches for enhanced value and market positioning.

Conclusions

Silver Lake’s consideration to privatize Endeavor is influenced by multiple elements such as the PE fund’s deep-rooted association with the company, the evolving trends in the entertainment sector, Endeavor’s significant scale and influence, the latter’s lower valuation in public markets, and a strategy aimed at realigning financial and operational goals to foster long-term growth and enhance value. Since 2012, under Silver Lake’s ownership, Endeavor has not only grown significantly but also diversified, mirroring a broader industry inclination towards consolidation and strategic reorientation. This transition from a talent agency to a key player in sports and entertainment uniquely situates Endeavor within the industry landscape.

The deal underscores several critical insights. Firstly, it demonstrates the substantial impact of market perceptions on a company’s strategic choices. Then, it shows the necessity for companies to dynamically adjust and react to evolving industry trends and competitive pressures to preserve their market standing. Finally, the decision highlights the importance of timely and decisive actions, such as considering privatization, particularly when a company faces challenges like declining stock performance.

Overall, Silver Lake’s investment thesis likely centres on the belief that Endeavor has untapped potential that can be realized away from the public eye. Hence, by taking the company private, the fund may aim to strategically reposition Endeavor away from the short-term earnings expectations of public markets, enabling a focused execution of long-term growth initiatives that could enhance the company’s intrinsic value.

- https://www.reuters.com/business/ufc-owner-endeavor-announces-review-strategic-options-2023-10-25/

- https://www.silverlake.com/portfolio/endeavor/

- https://www.pehub.com/silver-lake-invests-in-william-morris-endeavor-entertainment/

- https://finance.yahoo.com/quote/EDR/

- https://www.endeavorco.com/story/

- https://www.capitaliq.com/CIQDotNet/company.aspx?companyId=614784871

- https://www.businesswire.com/news/home/20231025566368/en/Silver-Lake-Considers-Take-Private-of-Endeavor

- https://www.ft.com/content/0b15fc20-0bbe-4b8c-b51a-29c04ab6e648

- https://ca.finance.yahoo.com/quote/EDR/history?p=EDR

- https://www.ft.com/content/0b15fc20-0bbe-4b8c-b51a-29c04ab6e648

- https://money.usnews.com/investing/news/articles/2023-10-25/ufc-owner-endeavor-announces-review-of-strategic-options

Comments are closed.