Written by Marc Dambach, Nikolaus Schmidt-Chiari and Sophie Schwalb | Editor: Daniel Semotan

Private credit has moved from the margins of global finance to its centre. What began as a post-crisis workaround for over-regulated banks has become a structural pillar of leveraged finance, reshaping the flow of capital across the United States and, increasingly, Europe. With global private credit assets surpassing $2.1tn in 2025 and Europe now accounting for roughly a quarter of that total, the shift is no longer cyclical but systemic. Regulatory tightening, changing sponsor behaviour, and new investment vehicles are driving the rise of a financing model that is faster, more flexible, and increasingly mainstream.

This article explores the structural drivers behind Europe’s private credit boom, the regulatory forces accelerating it, and the emergence of Business Development Companies (BDCs) and ELTIF 2.0 as mechanisms that could democratise the asset class for the next decade.

The Structural Shift

Private credit’s ascent began in the aftermath of the Global Financial Crisis, when Basel III forced banks to strengthen capital ratios and hold more equity against risk-weighted assets. Higher Common Equity Tier 1 (CET1) requirements made corporate lending significantly more capital-intensive for traditional banks, limiting their willingness and capacity to finance leveraged or complex loans. This opened substantial white space in the market, and private lenders stepped in.

Operating under lighter regulation and backed by committed funding capital, direct lenders offered faster execution, custom structuring, and reliable closing certainty. What started as a cyclical substitute soon became a core financing option for private equity sponsors. This shift was amplified by timing: record private equity dry powder of about $1.6tn raised before the pandemic went largely undeployed through COVID-19 due to uncertainty, and the subsequent interest-rate spike in 2022–2023 froze activity once more. With global rates now easing, end-of-life funds returning capital, and transaction pipelines re-opening, sponsor demand for private credit is accelerating sharply.

US Saturation, European Momentum

After more than a decade of rapid growth, the US private credit market has matured. Competition increased, spreads compressed, and underwriting became crowded. As returns normalised, global managers sought new frontiers, and Europe emerged as the natural next stage.

Europe offers several structural advantages:

- lower market penetration

- fewer competing funds

- and a highly regulated banking system that still dominates corporate lending

These conditions create recurring funding gaps that private lenders can fill with speed and certainty. As of 2025, Europe represents about $0.5tn in private credit AUM, nearly 25% of global totals, and the fastest-growing region worldwide. Fundraising trends are reinforcing this pivot: European-focused vehicles raised around $26bn in 2025 compared with just $9bn in the United States.

Supportive Monetary Conditions

The macro backdrop is shifting in favour of private credit. Since September 2025, the Federal Reserve has cut rates twice, bringing the federal funds range to 3.75–4.00%, its lowest point in three years. The Bank of England has maintained rates at 4%, with inflation easing to 3.8%. Lower rates reduce borrower pressure, stabilise valuations, and help revive private equity deal flow, all of which directly lift private credit volumes.

A Two-Track Market

As the industry expands, private credit is bifurcating into two parallel markets. Mid-market direct lending has become the dominant financing model for sponsor-backed companies, driven by relationship-oriented underwriting and execution certainty.

Meanwhile, large-cap financing increasingly dual-tracks between syndicated loan markets and private alternatives, with direct lenders now capable of underwriting multi-billion-euro transactions thanks to their scale and permanent capital partners.This structural divide marks private credit’s transition from niche strategy to mainstream asset class.

Regulatory Catalysts and the New Terms Landscape

Regulation is the single most powerful tailwind for private credit today. The final phase of the Basel III reforms (commonly referred to as Basel Endgame or Basel 3.1) is reshaping banks’ lending capacity across the US, UK, and EU.

Basel 3.1 and Rising Bank Capital Costs

Basel 3.1 recalibrates how banks calculate risk-weighted assets by imposing an “output floor”: internally modelled risk weights cannot fall below 72.5% of standardised measurements. Supervisors simultaneously narrowed the scope of internal models and increased standardised risk weights for corporate exposures and commercial real estate.

The result is simple: many loans now require significantly more core equity from banks. This raises the cost of bank lending and forces institutions to reprice, retrench, or tighten structures, therefore opening the door even wider for private credit funds that are not subject to the same capital regime.

Flexible Structuring: From Unitranche to Cov-Lite

With bank terms tightening, direct lenders compete on speed, certainty, and customisation. Unitranche loans, which replace complex multi-layered bank structures with a single consolidated facility, have surged in popularity. They remove the need for intercreditor negotiations, cut closing times dramatically, and eliminate market-flex risk.

On the larger end of the market, covenant-lite documentation is becoming more common. While mid-market deals still rely on maintenance covenants, large-cap transactions are increasingly structured with incurrence-only protections, giving sponsors flexibility while lenders compensate through pricing and stricter reporting terms.

Execution Certainty and Partnership Models

In the current environment, execution certainty often outweighs pricing. Private lenders’ ability to underwrite and hold loans without syndication risk has become a decisive advantage, particularly in competitive processes or time-sensitive acquisitions.

At the same time, collaboration between banks and private credit managers is increasing. Banks often retain relationship roles, providing revolving facilities or working capital lines, while private credit funds take the term loan or mezzanine risk. Significant risk transfer (SRT) transactions in which banks offload slices of portfolio risk to private funds are growing rapidly as a way for banks to manage capital under Basel 3.1.

Together, these forces reinforce a system in which private credit is not replacing banks, but reshaping their role in leveraged finance.

The Liquid Alternative: BDCs and ELTIF 2.0

As private credit grows, so does the question of who provides the capital and who can access the returns. In the US, this question was answered decades ago with the creation of Business Development Companies (BDCs), which transformed private credit from an institutional strategy into one accessible for retail investors.

What BDCs Do

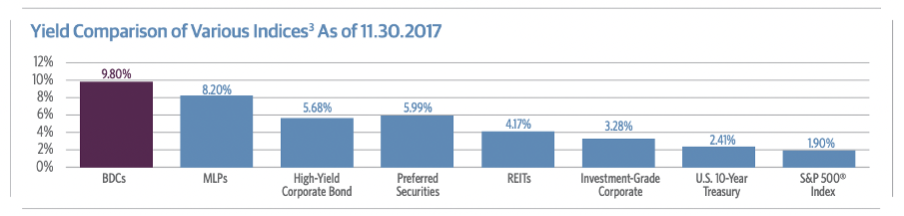

Created by Congress in 1980 to support small and mid-sized business financing, BDCs are closed-end investment vehicles that provide loans and occasionally equity to fast-growing or financially stressed companies. Their appeal lies in their high-yield income profile, as BDCs must distribute at least 90% of taxable income to maintain tax-advantaged status and their transparency as exchange-listed vehicles.

They are also heavily regulated: the SEC requires that at least 70% of assets be invested in US companies valued below $250m, and BDCs are subject to leverage limits and ongoing public disclosure obligations.

Prominent players include Ares Capital Corporation (ARCC), one of the largest BDCs globally, and Blackstone Secured Lending (BXSL), which focuses on first-lien senior secured loans with strong creditor protections. These vehicles offer public investors exposure to private loans while maintaining liquidity through stock-market trading.

Europe’s Answer: ELTIF 2.0

While Europe lacks a direct BDC equivalent, the revised European Long-Term Investment Fund framework, ELTIF 2.0, represents a major step toward democratising access to private markets. The updated rules reduce minimum investments, loosen portfolio composition constraints, and improve redemption flexibility, allowing retail and mass-affluent investors to allocate to private credit through regulated structures.

The impact is already visible. France’s “Industrie Verte” law has channelled €4.7bn into unlisted assets via ELTIFs, and by 2024, total ELTIF volume reached €20.5bn across more than 130 funds. Major US firms, including Ares, have launched ELTIF strategies to adapt their BDC-style lending approaches for European investors.

This development signals a structural shift: private credit is no longer an institutional niche but an increasingly mainstream asset class on both sides of the Atlantic.

Conclusion

The rise of private credit reflects big structural changes in global finance. Basel 3.1 continues to push banks toward lower-risk activities, while direct lenders step in with speed, flexibility, and the ability to absorb complex risk. Europe, long dominated by relationship banking, is now at the centre of this transformation, attracting global capital and reshaping its leveraged finance ecosystem.

At the same time, BDCs in the United States and ELTIF 2.0 in Europe are democratising investor access, turning private credit into a liquid alternative for a broader audience. These trends collectively point to a future in which private credit becomes not merely a substitute for bank lending, but a foundational component of global capital markets.

Bibliography

American Bankers Association Banking Journal. (2024). The Basel III Endgame Proposal: Yet Another Gift to Private Credit Funds. Retrieved April 1, 2025, from https://bankingjournal.aba.com/2024/07/the-basel-iii-endgame-proposal/

Bank for International Settlements – Basel Committee on Banking Supervision. (2017). Basel III: Finalising Post-Crisis Reforms. Retrieved April 1, 2025, from https://www.bis.org/bcbs/publ/d424.htm

Board of Governors of the Federal Reserve System; Federal Deposit Insurance Corporation; Office of the Comptroller of the Currency. (2023). Regulatory Capital Rule: Large Banking Organizations; Proposed Rule (Basel III Endgame). Retrieved April 1, 2025, from https://www.federalreserve.gov/newsevents/pressreleases/bcreg20230727a.htm

European Banking Authority. (2022). Guidelines on Significant Risk Transfer for Securitisation. Retrieved April 1, 2025, from https://www.eba.europa.eu/regulation-and-policy/securitisation/guidelines-on-significant-risk-transfer

European Commission. (2021–2024). CRR III and CRD VI Legislative Package. Retrieved April 1, 2025, from https://finance.ec.europa.eu/regulation-and-supervision/banking-and-finance/banking-union/capital-requirements_en

McKinsey & Company. (2024). Global Private Markets Review and Private Credit’s Next Act. Retrieved April 1, 2025, from https://www.mckinsey.com/industries/private-equity-and-principal-investors/our-insights

Carne Atlas. (2024). Private Markets Forecast. Retrieved April 1, 2025, from https://carnegroup.com

Guggenheim Investments. (2017). An Overview of Business Development Companies (BDCs). Retrieved April 1, 2025, from https://www.guggenheiminvestments.com

Investopedia. (n.d.). Business Development Company (BDC). Retrieved April 1, 2025, from https://www.investopedia.com/terms/b/bdc.asp

Preqin. (2024). Global Private Markets Report. Retrieved April 1, 2025, from https://www.preqin.com/insights/global-reports

Ares Capital Corporation. (2025). Investor Relations. Retrieved April 1, 2025, from https://www.arescapitalcorp.com

Ministère de l’Économie, des Finances et de la Souveraineté industrielle et numérique. (2023). Que contient la loi Industrie Verte? Retrieved April 1, 2025, from https://www.economie.gouv.fr/actualites/que-contient-la-loi-industrie-verte

Comments are closed.