Written by Victor Weinzirl, Naz Yuksel, Gaia Trapani and Boris Penev | Editor: Maciej Skorupka

The Return of the Corporate Break-Up

After a long era of empire-building, many corporations are now reversing course and breaking themselves apart. Corporate break-ups (including spin-offs, divestitures and carve-out deals) have surged as companies shed non-core divisions to simplify operations and focus on their core activities. In the United States alone, announced corporate break-up deals totalled roughly $725 bn by mid-2025, a jump of about 48% over the prior year’s pace.

With higher interest rates, weaker M&A activity, and decreasing investor appetite for IPOs, large corporates are rethinking how to create liquidity and value. At the same time, private equity funds are putting their record levels of dry powder to work (around $2.6tn), acquiring non-core divisions and transforming them into independent, profitable businesses.

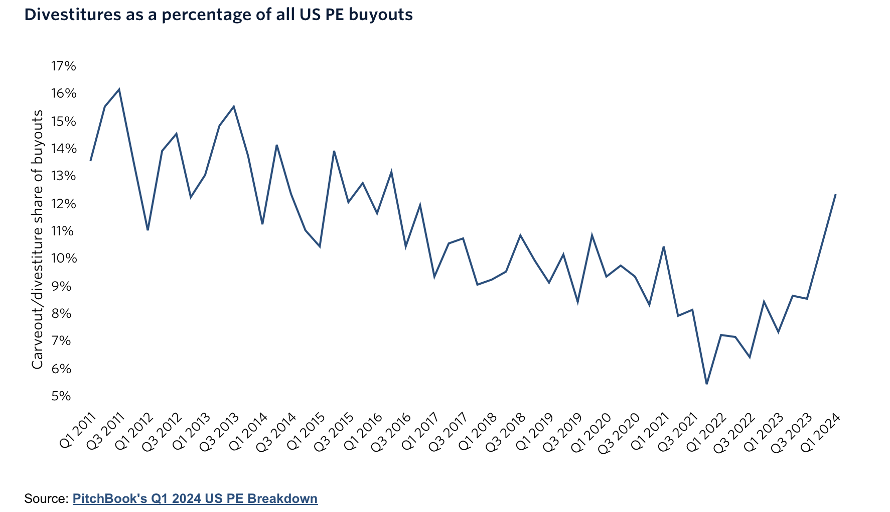

Carve-out acquisitions accounted for about 12.6% of all U.S. buyouts in early 2024, more than double their share from a 2021 low. Europe has seen a similar uptick, with carve-outs reaching 18.2% of deal value in Q3 2024, the highest level in years, according to Pitchbook.

The Anatomy of a Carve-Out Deal

Pre-Deal Planning and Strategic Rationale

Every carve-out begins with a clear strategic rationale. The first step is defining the carve-out entity – the business, division, or asset pool that will form the separated company. Management must choose between a legal-entity approach, where the carve-out mirrors existing legal structures, or a management approach, which reflects operational reality. This decision determines which assets, liabilities, and results appear in the financials and underpins the credibility of the deal for auditors, regulators, and investors.

Once scoped, management prepares carve-out financial statements showing the historical performance of the soon-to-be-divested unit. These must capture all direct and shared costs (HR, IT, legal, etc.) and comply with IFRS or US GAAP. That requires robust cost-allocation methods, mapping of intercompany transactions, and a clear view of how the business will operate on a stand-alone basis.

Structuring and Execution

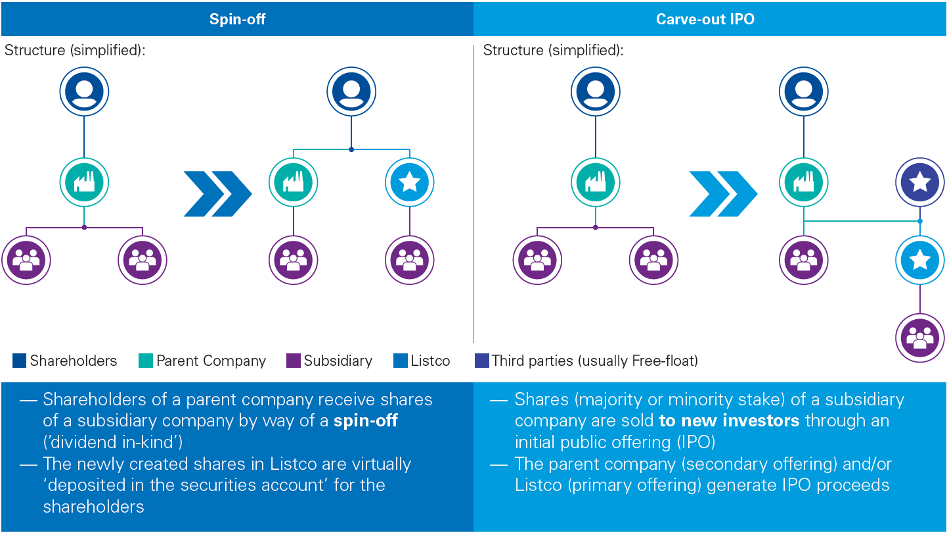

The core of any carve-out lies in structuring and execution. Transactions typically take three forms. In a spin-off, the parent distributes shares of the new entity – often called Listco 0 to existing shareholders on a pro-rata basis, creating no new capital but giving investors direct exposure to a focused business. In a carve-out IPO, the parent sells a minority or majority stake in the subsidiary to the public, raising funds for itself or the new entity; over 60% of carve-out IPOs are secondary offerings, monetising part of the parent’s equity while retaining control. Finally, hybrid deals blend both models, such as a private spin-off followed by an IPO or a dual-track process that preserves flexibility between listing and sale.

Execution is complex and resource-intensive. The process typically spans six to eighteen months and involves thousands of interdependent workstreams across legal, financial, and operational domains. Most successful carve-outs establish a dedicated Carve-Out Management Office (PMO) to coordinate activities, align stakeholders, and oversee critical functions such as IT separation, HR transition, tax structuring, and regulatory filings.

A defining feature of this phase is the Transitional Service Agreement (TSA): a contract specifying which services the parent will continue to provide, from ERP access to payroll, while the new entity builds its own capabilities. TSAs can be both a safeguard and a risk: poorly defined terms often cause cost overruns or operational disruption, while well-designed agreements ensure business continuity and protect value during the transition.

Post-Deal Transition and Stand-Up

In the final stage, or stand-up, the carve-out becomes a fully operational company. The focus shifts from separation to independence, building standalone systems, governance, and culture. This phase is risky; up to one-third of carve-outs fail to meet expectations because complexity is underestimated. Common pitfalls include data migration failures, duplicated costs, and loss of key talent. For private equity owners, stand-up often means “building the missing middle”: creating finance, IT, and procurement functions from scratch while keeping performance on track. Done well, however, the payoff is clear: well-executed carve-outs can deliver EBITDA margin gains of 10-20% within two years, showing that disciplined execution is as important as strategic intent.

The Drivers Behind the Carve-Out Boom

Corporations are increasingly using carve-outs to simplify and sharpen their strategy. After the pandemic, many conglomerates recognised that diversification diluted competitiveness; by divesting non-core or underperforming units, they can redeploy capital toward high-growth areas such as digital infrastructure, renewable energy, and AI. Activist investors have reinforced this shift, urging boards to separate distinct business units and present clearer, more focused value stories to shareholders.

This strategic realignment is unfolding against a challenging macroeconomic backdrop. Volatility, inflation, and high interest rates have raised the cost of holding capital-heavy divisions, while tighter credit markets have made traditional financing harder to access. As a result, carve-outs have become an attractive way to inject liquidity, reduce leverage, and raise capital without diluting equity.

Moreover, regulatory scrutiny in sectors such as technology, energy, and telecommunications has encouraged pre-emptive separations to satisfy antitrust concerns and ESG transparency requirements.

The result is a dual trend: corporations seek resilience and focus, while investors pursue opportunity. Private equity firms, sitting on more than a trillion dollars of dry powder globally, are eager acquirers of “non-core” assets that can be revitalised through operational improvements.

Technology is reshaping both the purpose and execution of carve-outs. Rapid digital transformation and automation have shortened product lifecycles and forced companies to rethink how portfolios create value. Many now separate legacy operations from high-growth digital units, such as AI or fintech divisions, to unlock focused investment and innovation. Carve-outs have become strategic tools for managing technological change and enabling both legacy and digital businesses to thrive independently.

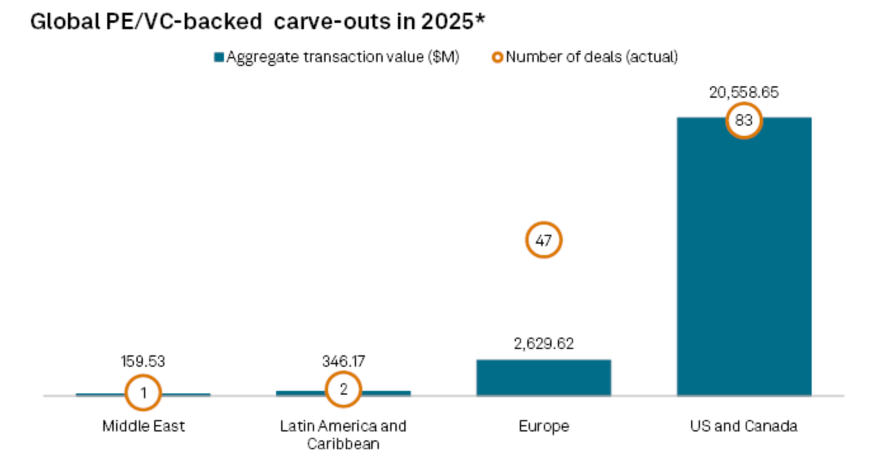

Regionally, carve-out activity is accelerating worldwide. North America leads on the back of strong deal volumes; Europe is also growing, with carve-outs representing nearly one-fifth of private equity deal value as regulatory and cost pressures mount. In Asia, particularly Japan, rising M&A momentum and corporate reform are setting the stage for a surge in carve-outs

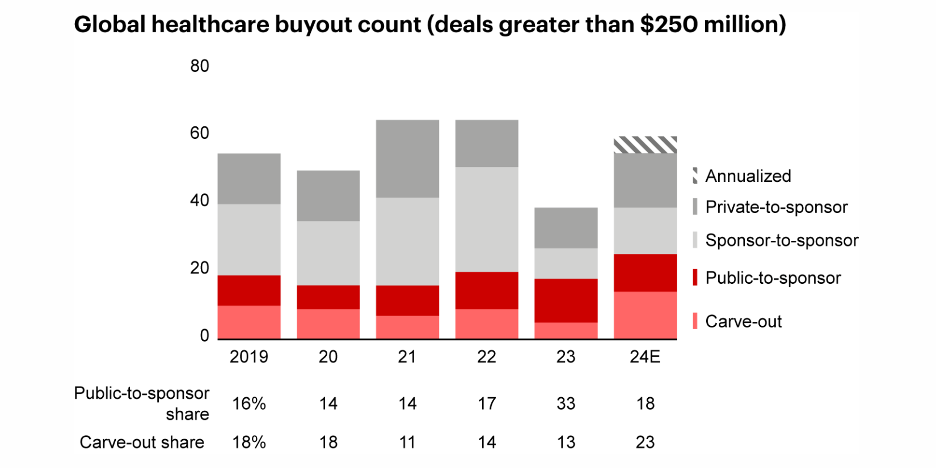

While financial services, B2B products, and tech have been traditionally strong sectors for carve-out deals, on the graph below, it can be observed that this deal structure is becoming increasingly important for other sectors such as healthcare.

Case Study

In July 2024, Telecom Italia sold its fixed-line network and wholesale unit, NetCo, to a KKR-led consortium, concluding a separation process that had run for several years. The deal, valued at up to €22.0 bn including earn-outs, is expected to cut net financial debt by about €14.2 bn after post-closing adjustments. For Telecom Italia, the sale marks a turning point, freeing it to reshape its operating model, focus on services, and compete more effectively in the Italian market.

A key step came when the European Commission granted unconditional approval on 30/05/2024, confirming that the acquisition would not harm competition in wholesale broadband. The decision also endorsed a long-term master services agreement between Telecom Italia and NetCo, which governs how the two companies will work together after separation and sets their respective responsibilities.

Ion Analytics highlighted the deal’s high execution complexity. Fully separating critical network infrastructure from the remaining service business required intricate technical work and negotiations with multiple stakeholders, including the Italian government, given NetCo’s strategic role. The transaction also demanded careful handling of labour and regulatory issues. From a private-equity perspective, it shows that firms like KKR are willing to manage such complexity when assets are large, capital-intensive, and positioned for long-term transformation.

The NetCo carve-out thus illustrates more than a headline valuation. It embodies key themes in today’s European carve-out market: strategic refocusing, balance-sheet repair, and intensive regulatory engagement, linking the broader corporate break-up trend with the practical realities of executing a major separation.

The Future: From “Carve-Out” to “Carve-Up”

Looking ahead, the carve-out boom might soon evolve into a broader “carve-up” phase, marked by multiple spin-offs and break-ups. Instead of one-time divestments, companies are now pursuing multiple carve-outs, sometimes one after another, sometimes all at once. We may see PE buyers acquiring multiple divisions from the same parent company over a series of transactions, effectively dismantling conglomerates into focused parts. Notably, when General Electric announced plans to split into three companies, private equity firms quickly began circling its most attractive divisions as potential acquisition targets.

At the same time, buyout firms are likely to initiate their own spin-offs within their portfolios. Many are carving out pieces of the companies they own and selling those divisions to specialised investors or new funds that can maximise their value. This trend is already underway: private equity sponsors have begun using continuation funds and similar vehicles to spin off high-performing units for further growth (Grant Thornton). In short, secondary carve-outs and new deal structures are becoming increasingly common, narrowing the gap between corporate divestitures and private equity transactions.

Summary

After years of expansion and building of diversified business portfolios, corporations are increasingly looking for opportunities to reorganise their business through spin-offs, divestitures, and carve-outs with the aim to refocus on core strengths and unlocking value. The fact that there are over $725 billion in U.S. break-up deals by mid-2025 and private equity firms deploy $2.6 trillion in capital demonstrates a possible response to high interest rates, tight credit, and investor demand for clarity. Through carve-outs, the companies can easily streamline operations while PE buyers can transform non-core assets into profitable stand-alone businesses, such as the example with Telecom Italia’s NetCo sale to KKR. Moreover, diversification leads to higher costs, so specialisation in core business practices allows firms to reinvest in digital infrastructure, AI, and renewable energy.

In the future, corporate carve-outs will become more dynamic as companies will continuously reshape themselves to stay competitive and adaptive. One possibility is that instead of being static conglomerates, firms will operate as networks of independent business segments that can spin off, merge, or realign depending on market conditions.

Bibliography

Dissecting Public Carve-Outs: What Are the Dynamics of a Successful Transaction?; https://assets.kpmg.com/content/dam/kpmg/xx/pdf/2020/10/dissecting-public-carve-outs.pdf

Guide to Preparing Carve-Out Financial Statements; https://www.ey.com/content/dam/ey-unified-site/ey-com/en-us/technical/accountinglink/documents/ey-co00545-181us-05-14-2024.pdf

The Alpha Factor in Private Equity Carve-Out Deals; https://www.mckinsey.com/industries/private-capital/our-insights/operations-the-alpha-factor-in-private-equity-carve-out-deals

Unlocking Value Through Corporate Carve-Outs; https://www.petiole.com/en/insights/articles/carve-outs

PE Carve-Out Deal Value Rises as Companies Refocus on Core Operations; https://www.spglobal.com/market-intelligence/en/news-insights/articles/2025/6/pe-carveout-deal-value-rises-as-companies-refocus-on-core-operations-90541554?utm_source=chatgpt.com

Wall Street Is Falling in Love With the Corporate Breakup. Here’s Why; https://www.fastbull.com/news-detail/wall-street-is-falling-in-love-with-the-4342688_0

Carve-Outs for Private Equity: High Stakes, Higher Returns; https://www.fticonsulting.com/insights/articles/high-stakes-higher-returns-carve-outs-private-equity

Wall Street Is Falling in Love With the Corporate Breakup; https://consent.yahoo.com/v2/collectConsent?sessionId=3_cc-session_b7b90245-6d82-436a-a5ff-93fb53b800c4

Private Equity Buyers Plot to Carve Up General Electric; https://www.ft.com/content/d2c421bd-0ad2-403b-a585-7b4f52a3abf7

PE Exit Strategies: Continuation Funds and Carve-Outs; https://www.grantthornton.com/insights/articles/pe/2025/continuation-funds-and-carve-outs

TIM: Sale of NetCo to KKR Completed; https://www.gruppotim.it/en/press-archive/corporate/2024/PR-Closing-NetCo-1-luglio.html

KKR Wins EU Nod for $24 Billion Telecom Italia Fixed-Line Network Deal; https://www.reuters.com/markets/deals/eu-clears-kkrs-24-bln-telecom-italia-fixed-line-network-deal-2024-05-30/

KKR’s Acquisition of NetCo; https://ec.europa.eu/commission/presscorner/detail/en/ip_24_2993

Tangled: TIM’s NetCo Troubles Signal Carve-Out Conundrum; https://ionanalytics.com/insights/mergermarket/tangled/

Comments are closed.