By Francesco Marchetti, Henrique Bento and Valerio Bellandi

Japan’s public stock market has long been marked by low valuations. This persistent “Japan discount” is now starting to fade. Japanese equities recently surged to their highest level in 33 years, reflecting renewed investor confidence. The market is becoming increasingly attractive to private equity investors, driven by better corporate governance, supportive macroeconomic trends, and a growing willingness among Japanese firms to pursue asset sales and restructurings.

Some of the world’s largest private equity funds have begun reallocating capital to Japan, and a recent industry survey by Bain ranked Japan as the fourth most attractive developed market for private equity investments (after the US, Western Europe and the UK). At the same time, Japanese corporations are increasingly open to selling non-core business units or even going private.

Regulatory Environment

A key driver of this shift has been Japan’s corporate governance reforms. The Stewardship Code (2014) and Corporate Governance Code (2015) pushed for greater board independence, transparency, and capital efficiency. Building on these foundations, in 2023, the Tokyo Stock Exchange began urging companies with low market valuations to improve capital allocation—an initiative widely welcomed by investors.

The TSE also introduced tighter listing criteria and transparency rules, including a requirement for top-tier “Prime” market firms to publish disclosures in English. These developments fostered a more investor-friendly culture. Activist investors increasingly collaborate with management to drive changes, including divesting unprofitable divisions or pursuing buyouts. As a result, Japan’s corporate environment has become far more conducive to private equity dealmaking.

Further building on this trend, the Japanese Financial Services Agency (FSA) has increased pressure on companies to unwind cross-shareholdings and return excess cash to shareholders. In 2024, nearly 70% of listed companies still lacked clear capital efficiency strategies, prompting further regulatory focus. These measures aim to align Japanese corporate behaviour more closely with global investor expectations and incentivise restructuring.

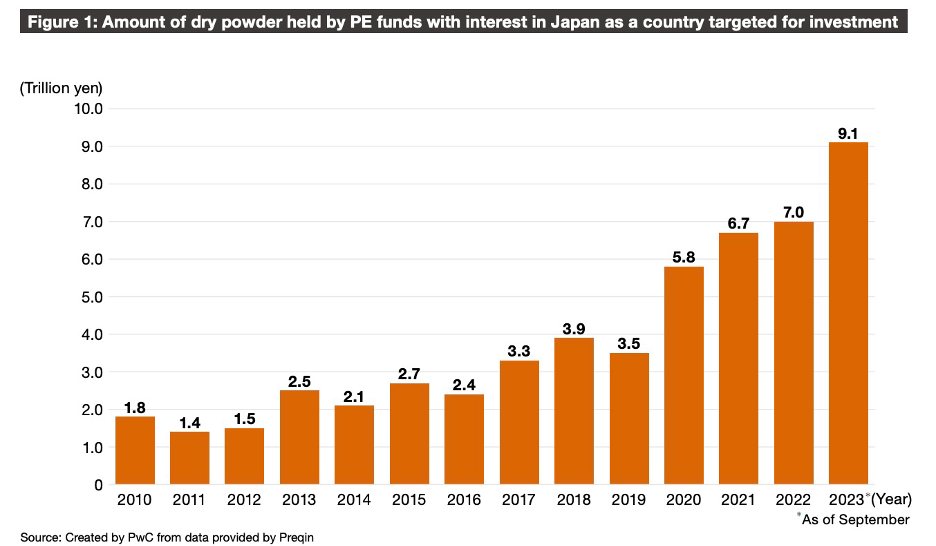

PwC Japan, Trends in Japan’s Private Equity Market and Related Considerations (2024).

https://www.pwc.com/jp/en/knowledge/thoughtleadership/trends-and-considerations-of-pe-in-japan2024.html

Key Transactions – Seven & I Holdings

These conditions have catalysed several headline deals, including KKR’s $4.4 billion buyout of Fuji Soft and the proposed $39 billion acquisition of Seven & I Holdings by Canadian retail giant Alimentation Couche-Tard (ACT). If successful, the latter would be the largest foreign-led acquisition of a Japanese company, testing Japan’s evolving M&A environment.

Seven & I, a sprawling conglomerate spanning convenience stores, hotels, and parking, sought to block the bid. The company applied to be classified as “core infrastructure” under the Foreign Exchange and Foreign Trade Act, subjecting the deal to direct finance ministry oversight. Despite recent reforms, this highlighted ongoing reluctance within Japan’s public and corporate sectors to allow foreign ownership of major firms.

The founding Ito family, still influential in company leadership, opposed the takeover and proposed a $58 billion management buyout (MBO). This bid failed due to funding difficulties, even as Apollo considered a $9.5 billion equity investment and KKR showed interest. The MBO’s failure underscored Japan’s still-limited appetite for dramatic ownership changes, even among progressive firms.

To fend off the bid, Seven & I carved out several businesses into a new holding company, York Holdings. In March 2024, Bain Capital acquired a 60% stake for $5.5 billion and plans further M&A and a listing within three years. Other private equity firms, including KKR, Blackstone, and EQT, also expressed interest in participating. The takeover saga continued, with ACT increasing its offer to $47 billion in October 2024. As of April 2025, discussions are ongoing, and both parties are exploring the divestiture of thousands of U.S. convenience stores to ease antitrust concerns. The still unresolved deal has already cemented its role as a case study in Japan’s changing corporate landscape.

Beyond Seven & I, other notable deals have reinforced the shift. For example, KKR’s acquisition of Hitachi Transport System for approximately $5.2 billion in 2023 marked a rare large-scale buyout of a logistics group with strong domestic ties. Similarly, Toshiba’s ongoing privatisation saga, which drew interest from multiple global PE players, has reflected both the complexity and scale of opportunities now open in Japan.

Drivers Behind the Uptick in PE Activity

Five primary drivers are behind the surge in private equity activity in Japan:

- Valuation Gaps – Japanese equities have long traded at discounts relative to other developed markets, often due to cautious governance and resistance to change. However, the factors that once suppressed valuations—like excess cash and reluctance to restructure—are now viewed as fixable inefficiencies, drawing in investors.

- Reform Momentum – Governance reforms have significantly enhanced board independence and capital efficiency. In 2023, the TSE took this further by requiring low-performing companies to improve their returns on capital, strengthening the business case for PE-backed restructurings.

- Foreign Capital Inflows – Global investors, facing elevated valuations and geopolitical uncertainty elsewhere, are turning to Japan. U.S. and European PE funds are particularly active, bringing capital and operating expertise to unlock value.

- Favourable Interest Rate Environment – While global interest rates remain high, Japan’s rates have remained comparatively low, making leveraged buyouts more financially viable. The Bank of Japan’s cautious approach to tightening further incentivises capital deployment in Japan.

- Sectoral Tailwinds – Certain sectors—like IT services, healthcare, and consumer goods—show strong earnings momentum and operational leverage. Deals like Bain’s acquisition of Evident, Olympus’s former scientific instruments unit, for $3.1 billion in 2022 illustrate the opportunity in sector-specific carve-outs.

Implications & Outlook

This trend has several implications. First, corporate governance has markedly improved, making Japanese firms more appealing to foreign investors. Enhanced transparency and accountability offer confidence to shareholders and acquirers alike.

Second, there has been a notable increase in carve-outs and take-privates as companies seek to boost shareholder value. Businesses are shedding non-core assets, and many underperforming subsidiaries are being divested to private equity firms, enabling parent companies to streamline operations. Third, shareholder activism is gaining traction. Foreign and domestic activists are pushing for better returns, more strategic focus, and leaner balance sheets. This creates more dynamic boardroom environments and opens the door to M&A activity.

Looking ahead, competition for quality assets is expected to intensify. As more funds target Japan, valuations may rise, prompting firms to be more selective. However, those that move quickly and with local insight may still capture attractive opportunities. Domestic institutional investors, such as pension funds and insurance companies, also play a growing role. They increasingly view private equity as a viable asset class. Their entry will deepen Japan’s capital markets and may spur further interest in alternative investments.

Lastly, cross-border deal structures are becoming more sophisticated as foreign firms partner with domestic sponsors to navigate regulatory complexity and cultural nuances. Recent deals have also included minority stake purchases and joint ventures, offering flexible pathways into the Japanese market. In short, private equity is developing in Japan through a successful interaction cycle between government reforms, private investment opportunities, and market response. This trend appears to be sustainable and likely to accelerate in the near future.

Bibliography

Bain — Asia-Pacific private equity shows green shoots of recovery, https://www.bain.com/about/media-center/press-releases/20252/asia-pacific-private-equity-shows-green-shoots-of-recovery/#:~:text=Similarly%2C%20limited%20partners%20,1%20globally

CFA Institute — Shareholder activism in Japan, https://blogs.cfainstitute.org/investor/2020/06/23/shareholder-activism-in-japan/#:~:text=The%20Corporate%20Governance%20Code%20,been%20targeted%20by%20activist%20shareholders

Newton Investment Management — Japan: investment implications of corporate governance reforms, https://www.newtonim.com/us-institutional/insights/blog/japan-investment-implications-of-corporate-governance-reforms/

Wellington Management — Activism: history and evolution in Japan, https://www.wellington.com/en-us/institutional/insights/activism-history-and-evolution-in-japan#:~:text=Unlike%20during%20the%20first%20wave,management%20reforms%2C%20such%20as%20divestitures

Financial Times — Seven & I facing growing investor unrest, https://www.ft.com/content/017b9828-7a0c-414b-aefe-a849e9bc4a29

Financial Times — Japanese M&A enters new phase, https://www.ft.com/content/5be5dee4-4005-4403-a605-fe226a0d0007

Financial Times — Japanese retail under pressure from foreign bids, https://www.ft.com/content/5a4709fc-82a6-450c-b078-fab838b570e5

Financial Times — Resistance to foreign takeovers in Japan, https://www.ft.com/content/be604c62-c691-44d6-9a0e-8ce7cfde9608

Financial Times — Ito family’s role in Seven & I bid, https://www.ft.com/content/4fac52b2-1be4-457e-97f9-74e71cb76dd3

Financial Times — Seven & I opens talks with ACT, https://www.ft.com/content/52dcc64f-aae5-4d4b-907a-a25c1d5882db

Financial Times — Japan’s regulatory review intensifies, https://www.ft.com/content/06fee706-8743-4df0-a3d1-5d8a2e504f8f

Bloomberg — Apollo weighs $9.5 billion stake in Seven & I management buyout, https://www.bloomberg.com/news/articles/2025-01-10/apollo-weighs-9-5-billion-stake-in-seven-i-management-buyout

Financial Times — PE firms circle Japanese retail assets, https://www.ft.com/content/aa51ddce-3930-49ae-9f99-e6e629ada7ec

PE Insights — Bain Capital plans IPO for Seven & I’s supermarket business within three years, https://pe-insights.com/update-bain-capital-plans-ipo-for-seven-is-supermarket-business-within-three-years/

Comments are closed.