By Tommaso Pietromarchi and Nicolas De Lacerda Bregantim

Foreword

Manuel Catalano is the current Executive Deputy Chairman of Armònia SGR, an Italian Private Equity fund that invests in leading Italian SMEs, mainly operating in manufacturing and service sectors. They specialize in high-quality local products, otherwise known as “Made in Italy”. These sectors helped the Italian economy keep up its competitiveness, acting as a primary growth driver. The fund focuses on value creation through a buy-and-build strategy for the overwhelmingly SME-centric domestic Italian market.

Manuel graduated from Bocconi, attending a five-year course in economics and social disciplines, tailored to statistics and econometrics. After serving as officer in the Italian Army, he began working for Morgan Stanley in the M&A department. He then pursued his MBA at Insead and left with a job at McKinsey. One year later he was hired by the prestigious holding Fininvest as a manager. Subsequently, he co-founded the first significant Private Equity firm in Italy, named Clessidra SGR, where he worked for 18 years, contributing to the fund raising and investment of approximately € 3 bln. Finally, in 2021, he joined Armònia, another Private Equity fund, where the investment focus, similarly to Clessidra, is still on Italian companies.

Based on your experience with the Private Equity market in Italy, can you offer any insight on the landscape of the current market as you see it?

The current environment is tough. After 10 years of “bonanza,” we face more complex issues. Fundraising, investment, and divestment processes are slowing down: fundraising is down approx. 35% compared to previous years. Investment activities are slowing significantly, being 70% less when compared to 2022. Also, the divestment process is seeing similar challenges, being down 40% of what it used to be.

Investors are facing what is called “the denominator effect”: Overexposure to private assets as a result of a slowdown in activity and funds inflow. Because of that, they’re not committing to new equity or new investments, mainly focusing on re-ups.

My outlook is that the market is cyclical; Look for example what happened in ‘93, 2000, and 2008. If in 2024 we experience lower interest rates this will trigger new exits and distribution, driving new commitments to funds that will drive recovery; it is all part of the cycle. With the decrease in return from fixed income, institutional investors such as pension funds, will increase their exposure to private assets.

Can you expand on the Italian Private Equity market, what are its key characteristics, and what differentiates the Italian market from other more developed Private Equity landscapes?

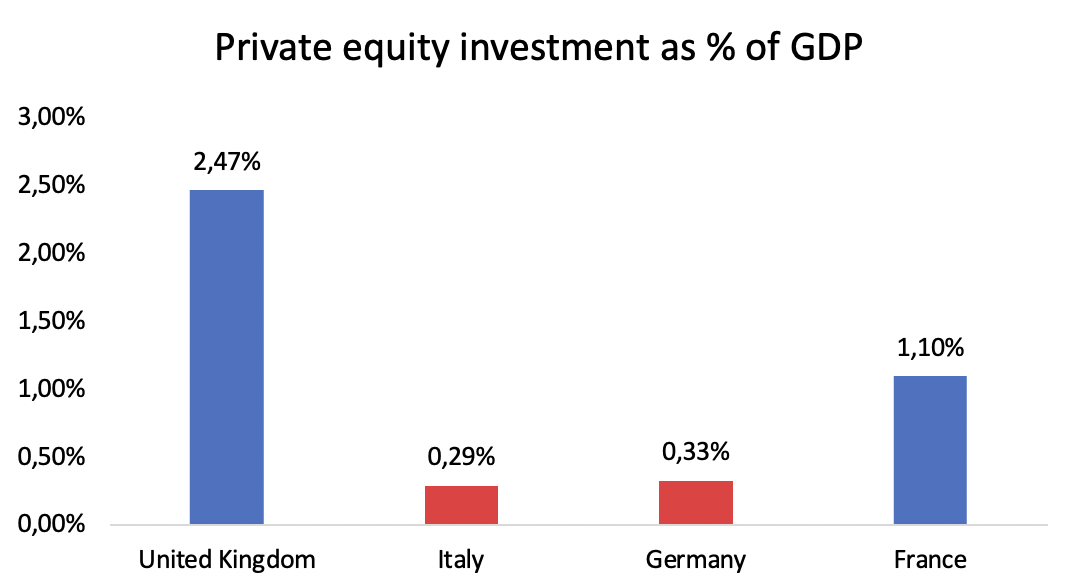

My view is that the Italian Private Equity market is still under-penetrated. When we compare Italy to the UK, the most advanced European economy in terms of Private Equity, we observe a stark difference in Private Equity investments as a percentage of GDP. Italy and Germany are roughly at 0.3%, France holds 1.1%, and the UK boasts 2.5% of Private Equity investments. When we consider the fact that the UK’s GDP is roughly a third bigger than ours, we quantify how much of a bigger role Private Equity plays in the UK’s market over Italy.

This underdevelopment in the market presents a growth opportunity in Italy. Especially when considering the overabundance of small and medium enterprises compared to other countries. The 3.6m SMEs compared to Germany’s 2.5m, means our economy is fundamentally driven by SMEs and family-owned companies. Usually, this characterizes high growth potential and consolidation opportunities as it is characteristic of less developed economies.

Italy has the largest portion of export-oriented companies, we always rank first or second in specific sectors in terms of export orientation. For example, Italy is one of the top three world exporters of clothing, leather products, non-electronic machinery, electronic components, textile ranks, transport equipment, and basic manufacturers. We always compete with China and Germany. Making it an incredibly attractive market for product equity funds.

I’ve been working in this market for over 20 years now, and I have concluded that there is an immense opportunity to create larger groups through a buy-and-build strategy. Which will characterize the future growth of the Italian Private Equity market.

Statista – Private Equity as a share of GDP in European countries 2022

What is the approach to value creation in the market with these quintessentially Italian products and businesses?

Our first goal of investment through SMEs is to help grow the company in ways the entrepreneur is unwilling or unable to do alone. Our primary role is to act as financial partners to support the company’s growth phase. Our second step is to attract management; financial sponsors that own a majority stake in a company have an advantage in attracting talented management. By aligning managers with the proper incentive scheme, we can attract top managers in a way that an entrepreneur could not.

Then the most important aspect is to have a clear idea of potential targets to pursue a buy-and-build strategy. The success of the investment is largely dependent on the selection of the acquired company. Analysing potential targets that can be acquired in a strict time frame of two or three years can be troublesome. Many foreign funds were pursuing buy-and-build 20 years ago, so learning from them plays a key role in our strategy. Another important aspect is considering ESG implementation. Nowadays ESG is key both for your portfolio and when looking at exit opportunities, as many international funds and industry shareholders ask for an ESG strategy.

ESG is tricky to implement for an entrepreneur alone, on the other hand, it’s easier for institutional investors to be very clear about the implementation deadlines, and objectives. Our carried interest is linked to the ESG objectives, so we also align management and the target companies’ incentives similarly.

Aifi-PwC 2023

Can you touch both on the buy and build strategy, and on the ESG investments process, and explain what changes are needed for the Italian markets to catch up to the foreign markets?

We first analyse the sector we want to invest in. You cannot implement a buy-and-build strategy if you invest in luxury brands because all you acquire is the brand, in that case, the focus shifts to the retail network, opening new stores, and so on. In other sectors like machinery, food, or service companies it’s much easier to implement, buy and build. These acquisitions are facilitated through a financial majority owner in a market like Italy as you often have many rival companies that refuse to talk to each other. Sometimes you realise on the field that the rivalry among Italian entrepreneurs is deeply rooted in the historical backdrop of medieval times. Stemming from the medieval era, where independent city-states fiercely competed for power and resources, this spirit of competition has persisted through the centuries. Modern Italian entrepreneurs, heirs of this legacy, navigate in a dynamic business environment marked by intense regional competition.

Funds have the advantage of not being subject to this rivalry, for example, last year we sold the most active company in the pharmaceutical industry. We did over six acquisitions in two years, this would not have been possible without us facilitating as a third party. Executing all these acquisitions was laborious considering the amount of target finding and due diligence needed for these deals to take place. But this is key when you pursue a strategy that targets returns over 20%. Since it is very difficult to pursue organic growth and achieve these rates of returns it must be done through acquisition.

In terms of ESG, we run two funds, one of which is Article 6 and the new Article 8 fund which has strict ESG objectives that need to be achieved. ESG introduced an increase in proper due diligence to make sure the assets meet these goals, 20 years ago the due diligence in the Italian market was not this strict.

Then together with some consulting companies we elaborate an ESG plan and align the management team’s incentives, which we monitor every year with our short-term and long-term objectives. This is fundamental for selling assets for funds, as it is one of the first things they look at.

Analysing the funds in the Italian market, you spoke about the success that mediation brings for the buy-and-build strategy. What differentiates a winning investment in that landscape, through this concept of buy and build, and mediation between partners?

I believe mediation is key for the strategy we pursue and, most importantly, it is crucial to know the people you’re dealing with. I think this is a “people business” because it’s a commodity, the process itself is a commodity, buying due diligence from a consulting firm being a clear example of this. What’s relevant is the people you’re dealing with, the seniority they have, their heritage, and the languages they speak. The language barrier is a peculiar phenomenon in our country, with many entrepreneurs not speaking English or, if they do, without the proficiency required to work in an international sector such as this one. Entrepreneurs want to deal with people who relate in the same way, which is not very common in international funds, particularly if you deal with Italian SMEs.

On top of this, you also need seniors because the youngest entrepreneurs are 45-50, but the oldest is up to 75-80 years old and, as I said before, they want to deal with people with seniority, they want to talk to people with “grey hair”. Lastly, it’s fundamental to have people who work in the office or that can be available in two, or three hours at the maximum. This is also fundamental when you pursue B&B strategy because, again, you need to be local to understand the differences between a company located and operating in Valle d’Aosta with another in Puglia, for example. This is why I think there is still room for new domestic funds.

The Italian Private Equity market, to a certain extent, reflects Italian culture. Looking forward, how do you see the market evolving, and specifically, which sectors do you think are going to attract the most international investors? And which is more appealing for domestic funds?

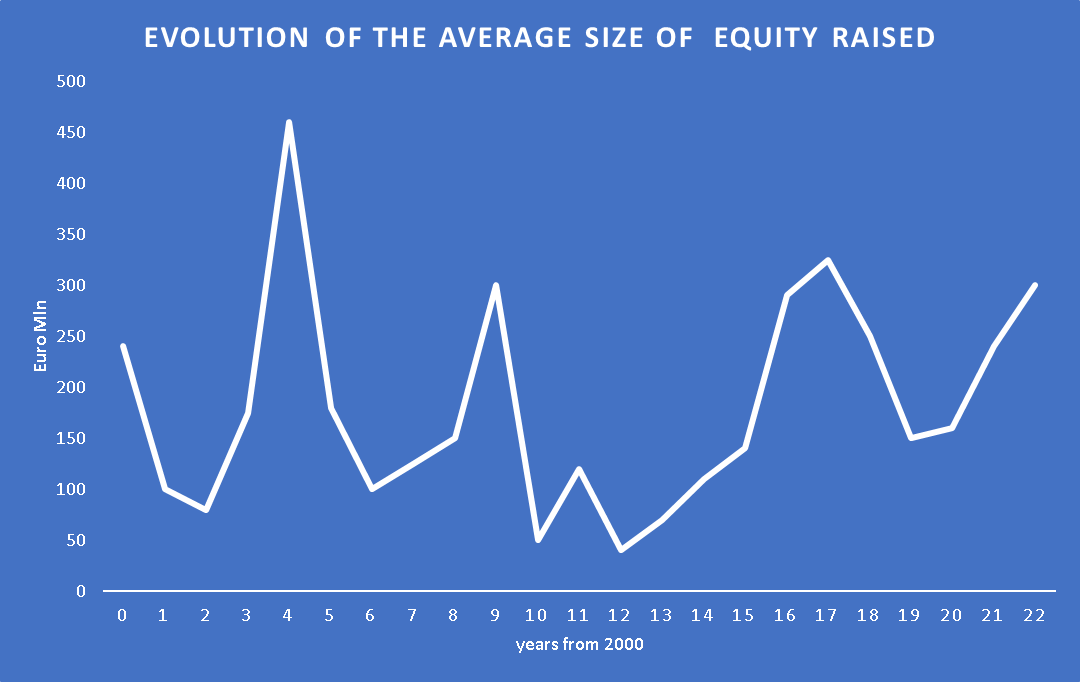

I think international and domestic funds are looking at the same assets. It’s a question of size because the average size of domestic funds is not so large. We are looking at an average of €300m of committed capital, on the other hand, international funds have a significantly larger spot. To this extent, I think we aim for different targets in terms of size, but in terms of sectors, the targets are the same. I mean, we concentrate on food, machinery, ICT, and recently there has been an increasing focus on schools and education. The main difference is internal specialization. International funds work on verticals, so they have specialized teams. As a matter of fact, in the payment industry, they have a special team that has closed deals across the world, and this is why I believe it is so effective. When you buy big assets, you require very strong expertise, which comes from teams that are working on similar deals. For example, in the US and UK or the Nordics, we do not have a specialization, but we can work on primary deals, which are non-structured, family-owned companies. We work to structure them, to manage them to adopt a buy-and-build buy strategy, and then sell these assets to larger funds, which are mainly international.

Aifi-PwC 2023

Due to the recent additional difficulties in fundraising in the Italian market, how do you think this will affect the market going forward in future years? Do you think this is also part of the business cycle or does this come with longer-term negative implications?

In the past, in the recessionary cycles, many international funds left Italy. They closed the Italian offices and focused on the core markets. Then we showed up in Italy when the market was booming again. This is to say international funds have always considered Italy as a marginal country and I think this has now changed. They have learned that the Italian market is important despite the volatile political stability and the slow economic growth. Because the niche, I mean the part of SME companies continues to grow, they may be slowing down at times, but the core of this market is solid and it’s growing, representing a clear opportunity.

The attitude of entrepreneurs towards Private Equity has changed a lot over the past 20 years: at the beginning, we were perceived as what was described in “Barbarians at the Gate”, now it’s a completely different environment because we are seen as an alternative to support the funding needs of companies. I mean, nowadays the bank debt is almost closed or it’s very expensive. You cannot go public unless you have a big company. So, the real opportunity for entrepreneurs is Private Equity, and this is why I expect the market to recover.

There is not a big history of continuation in terms of funds because, if you look over the last 20 years, there have not been many funds lasting on the market. I expect to see a smaller number of players consolidating and running larger funds. I believe the market is missing a large domestic firm running funds amounting to 1b plus in asset management, being able to compete with the largest players. So again, I’m optimistic. I think institutional investors are increasingly focusing on the product equity market because they see that it’s part of their asset allocation strategy, as it’s happening in the Anglo-Saxon world. These international investors are now focusing more and more on private assets. Another major phenomenon taking place in the market is the creation of a domestic fund of funds, supported by Cassa Depositi e Prestiti. Regarding this last phenomenon, they push for thematic fund of funds where institutional investors, such as pension funds, invest, and then the funds do the selection of the investment operations. This is again, something that is providing efficiency to the market as it helps investors make the correct choice regarding which managers, they should focus on rather than investing directly by creating an investment team and so on. I think the market is shifting towards efficiency. It’s moving slowly, but I believe in the correct direction and through appropriate measures. The Anglo-Saxon world should be our goal, our reference point, and even though the path is long, we are making giant leaps towards this objective.

In 20 to 25 years. Do you see the presence of these large domestic funds in the Italian market?

I think we’ll see local funds moving internationally. I think we will lose the pure domestic funds, but we’ll see the creation of a sort of federation of local teams, backed by an international pool. We will see consolidation and the creation of global players.

Thank you very much, once again, for your time. Finally, we would like to ask what advice you would give to current Bocconi students wanting to learn about and break into the Italian Private Equity market.

We are very on the field, so it’s not easy for us to train people. What we do is we always hire people who already have two, or three years of experience, either in consulting or investment banking because they are very well-trained. I think that large investment banks and consulting firms provide very good training, and this is obviously where students should work hard to be hired. Joining a firm where the team is not too large and where you can directly complete and participate in deals is essential, as initiating or completing a deal is a completely different story than pitching or working on something that is not part of the implementation phase. My strongest advice is that it doesn’t matter if you move from a large firm (big name) to a smaller firm, the important thing is that this firm is effective and operative in terms of completing deals, acquisition, fundraising, portfolio management, as this is essential for growth. I mean many of our junior teams are hired by larger firms because they know we’ve been working on the field. They’re following two or three portfolio companies, managing a couple of deals every time, so it’s very demanding. You also need to manage your time very well because you’re taking part in many activities. Of course, this regards peak activity periods, such as year end and before summer break.

I think this is one of the most complete jobs. I worked in investment banking, then consulting, I’ve been working for a family company and then I moved to Private Equity. And I would say that this is probably the synthesis of all these kinds of jobs. You’ve got the financial part, you’ve got the consulting aspect, you’ve got the psychological aspect on how to deal with entrepreneurs and with family-owned business, you’ve got project management, which is very important. Every case and every investment are a different story. It’s like a case study you do at university. My advice has always been to start with a company that has a very good training centre because I think it’s still important to start with a company that helps new hires in terms of training, knowledge, and exposure to senior teams, which is not something that Private Equity funds can do.

Image – IMAGOECONOMICA

Comments are closed.