Written by Federico Lucarelli, Tristan Buckley, Niccolò Cintioli and Kristaps Vaivars

TREND FRAMING AND WHY IT MATTERS

Private equity funds have traditionally been built around a 10-year lifespan, with the standard timeline of acquiring a company, improving its operations, and exiting within a shorter timeframe. In recent years, exit timelines have lengthened, and in 2023, the average holding period for US and Canadian buyouts reached 7.1 years, and the conditions that would allow for faster exits have only partially improved since (Bain, 2025, S&P Global, 2025). IPO markets remain subdued, and while M&A activity has recovered in 2025, distributions to limited partners fell to 11.0% of net asset value in 2024, the lowest figure in over a decade (Bain, 2025). Continuation vehicles have become the industry’s answer to this problem. Nearly 75% of the world’s 50 largest general partners had used CV structures by the first half of 2025 (Jefferies, 2025). The adoption reflects a logical solution to the issue, as GPs retain ownership of assets with remaining upside, while existing limited partners have a clean exit option, resolving the tension without forcing a sale.

THE SECONDARY MARKET IN NUMBERS

The secondary market has grown sharply alongside the rise of CVs. Global transaction volume reached $162bn in 2024 and $240bn in 2025, reflecting a 45% year-on-year increase in 2024, and a 48% rise in 2025 (Jefferies, 2026). GP-led deals drove a large portion of that growth, reaching $115.0bn in 2025, a 53% YoY increase accounting for 48% of total secondary activity, with continuation vehicles representing 89% of that GP-led volume (Jefferies, 2026). Capital on the buyer side has increased alongside supply. Dedicated secondary capital reached $327bn in 2025, LP portfolios averaged 87% of NAV, and single-asset continuation vehicles transacted at or near par (Jefferies, 2026). These pricing levels argue against the view that CVs are distress-driven. Portfolio management, rather than liquidity pressure, now drives the majority of secondary transactions (Campbell Lutyens, 2025).

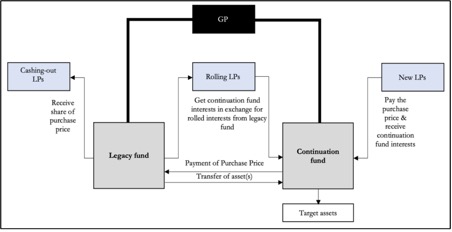

INTRODUCTION TO CONTINUATION VEHICLES

Continuation vehicles (CVs) are investment vehicles established by a private equity sponsor to acquire one (single-asset CVs) or more (multi-asset CVs) portfolio companies from an existing fund (legacy fund) managed by the same sponsor, typically as part of a GP-led secondary transaction.

Although the boundaries between the parties are not as clearly defined as in other transactions, the participants in the secondary transaction can be classified into two categories: the parties involved in the new acquisition and in the sale. Regarding the first category, the main actors are the new investors who will become the new limited partners (LPs) after the transaction occurs, the continuation vehicle itself and the general partner (GP). In contrast, on the sell side, there are the current LPs and, again, the GP, which plays a crucial role from both a buying and a selling perspective. In this regard, further analysis will be reported below. Apart from the parties mentioned, there are also the traditional parties which usually participate in private equity transactions, such as advisors and intermediaries.

THE RATIONALE OF CONTINUATION VEHICLES

To understand the rationale behind continuation vehicles, it is important to consider the different perspectives of the parties involved in the transaction. GPs usually use CVs to offset the mismatch between the investment horizon of private equity funds and the time that an asset requires to mature. In this regard, it often happens that the investment by the financial sponsor requires additional time to unlock its full potential. Therefore, in order to avoid a forced sale, which may damage the investors’ returns, general partners use continuation vehicles to fill this time gap and foster better future financial outcomes. In other instances, CVs can offer the opportunity to avoid a sale in adverse market conditions, which would lead to suboptimal valuation multiples.

From the LPs’ perspective, continuation vehicles represent an opportunity to liquidate their investments and materialise their financial results. Simultaneously, limited partners can join CVs, rolling their equity into the new fund, for the same motivations as GPs. Lastly, the secondary investors’ rationale is to invest in assets that have already showcased their potential during the investment horizon of the prior private equity fund and that, therefore, carry less risk. Through secondary investments, the new LPs can mitigate the J-curve.

THE PROCESS BEHIND CONTINUATION VEHICLES

The continuation vehicle process is a structured transaction which can be broken down into simple steps. First and foremost, the GP defines which asset or assets they want to retain. Then the CV is created, and an independent advisor is nominated to carry out a fairness opinion which is essential to initiate the price discovery phase and to defend the interests of LPs. The nomination of an independent party is critical to mitigate the conflict of interest generated by the presence of the general partner, both from the sell and buy side.

The market testing is carried out through the advisor, which contacts large secondary funds (anchor investors) to present the fairness opinion, indicate the portion of equity sought by the GP and solicit bids. At this point, each secondary fund submits its offer, stating how much it is willing to invest and at what valuation. After all offers are submitted, the final price is determined based on the most competitive bids that the GP deems acceptable.

At this stage, a few large secondary funds are selected as anchor investors, committing significant capital and validating both the valuation and the key economic terms of the transaction (such as management fees and carried interest). Their participation plays a crucial role in setting a reference point for the rest of the fundraising process. Subsequently, the process moves into a broader capital raise (bookbuilding), where additional, smaller investors are invited to participate on the terms agreed by anchor investors.

Lastly, LPs can decide whether to cash out, taking advantage of the opportunity to exit their investment, or to roll their equity into the new fund. The asset(s) are then finally moved to the CV.

Source: EGCI The rise of private equity continuation funds – Working Paper N° 733/2023

THE RISE OF CONTINUATION VEHICLES

The rapid rise of continuation vehicles is best understood as a structural response to a changing private equity environment rather than a temporary market trend. Over the past few years, traditional exit routes have become significantly less reliable. Higher interest rates, valuation mismatches between buyers and sellers, and subdued IPO markets have made it increasingly difficult for general partners to realise investments within the typical fund lifecycle. As a result, continuation vehicles have emerged as a flexible mechanism that allows sponsors to extend ownership of high quality assets without being forced into suboptimal exits.

At the same time, the needs of limited partners have evolved. Many institutional investors are facing liquidity constraints driven by the denominator effect, where declines in public market valuations have increased the relative weight of private assets in their portfolios. Continuation vehicles offer a structured solution to this tension. They allow existing investors to either exit and generate liquidity or roll over their investment into a new vehicle, preserving exposure to assets that may still have significant upside. This dual option has made continuation vehicles particularly attractive in the current environment, where liquidity is scarce but conviction in certain assets remains high.

Another important driver is the maturation of the secondary market. There is now a deep pool of specialised secondary capital with both the scale and expertise to underwrite these transactions. This has increased pricing efficiency and made it easier for general partners to execute deals at valuations that are acceptable to both selling and rolling investors. As a result, continuation vehicles are no longer viewed as opportunistic or distressed solutions, but rather as a standard portfolio management tool. This normalisation is reflected in transaction data, where continuation funds now dominate the GP-led secondary market, accounting for roughly 86 percent of total volume in 2025.

SINGLE & MULTI – ASSET CVS

Within this broader trend, an important distinction has emerged between single asset and multi asset continuation vehicles. Multi asset continuation vehicles involve the transfer of a portfolio of companies into a new fund, offering diversification and reducing asset specific risk for incoming investors. These structures were more common in the earlier stages of the market, as they closely resembled traditional fund dynamics and were easier to market to a broad investor base.

In contrast, single asset continuation vehicles focus on one specific company, typically a high-performing asset that the general partner believes still has meaningful value creation potential. These transactions have grown rapidly and now dominate the market. In 2025, single asset continuation vehicles represented approximately 53 percent of total GP-led volume, up from 48 percent in 2024 and materially higher than in earlier years. By comparison, multi-asset continuation vehicles accounted for around 33 percent of volume, highlighting a clear shift in market preference. The appeal lies in the clarity and alignment of single asset structures. For buyers, underwriting a single company allows for deeper due diligence and more precise valuation. For general partners, it provides the opportunity to concentrate capital and attention on their strongest investments. For existing limited partners, the decision becomes more transparent, as they can assess whether they wish to maintain exposure to that particular asset.

Source: Lazard Secondary Market Report 2025

The rise of single asset continuation vehicles also reflects a shift towards higher quality transactions. Rather than being used to manage weaker assets, they are increasingly deployed for top-performing companies that require additional time to reach their full potential. This has helped change market perception and attract larger pools of capital, reinforcing a virtuous cycle in which high-quality assets draw in sophisticated secondary investors.

THE INCENTIVE STRUCTURE IN CVs TRANSACTIONS

The most critical issue in CVs is undoubtedly the potential incentive misalignments between the parties of the transaction. In fact, GPs, beyond the noble motivations discussed in the paragraph above, may be driven by economic factors that could potentially undermine LPs’ interests.

Incremental fees may be a relevant driver for the GP. In fact, establishing a continuation vehicle allows the GP to earn management fees for an extended period. Although management fees in CVs are typically renegotiated at a discount, the decrease in percentage is often balanced by an increase in the value of the asset(s), given that the value of the asset(s) in the legacy fund tends to be lower than the value of the same asset(s) in the new fund. Furthermore, if a CV is created early in the life of the existing fund, it offers the opportunity to materialise the carried interest before the expiration of the legacy fund.

However, the most relevant incentive misalignment stems from the fact that the GP is committed to both existing LPs and secondary investors. These two groups clearly have opposite interests, as the existing LPs are interested in selling at the highest possible price, while the secondary investors are interested in buying at the lowest possible price. The conflict of interest is drastic when most LPs decide to cash out. On the other hand, if they decide to roll over their equity, they become, like the GP, both sellers and buyers, essentially mitigating the incentive misalignment.

Due to the role of the GP, who is committed to acting in the best interest of past and new LPs, the concern of existing LPs is that the GP will act in favour of entrant LPs, while the concern of entrant LPs is that the GP will favour the interests of existing LPs at the expense of secondary investors. Furthermore, another important concern is the possibility that the independent advisor may assess the asset(s) at a higher valuation in order to generate larger fees.

However, regardless of the tendencies of the GP, whether these are in favour of existing LPs or new investors, the general partner usually benefits from continuation vehicles. Firstly, as we have analysed, the GP accumulates fees and can materialise the carried interest earlier. Moreover, if the asset(s) are valued at a discount, the loss in carried interest will be offset thanks to the additional carried interest generated by the sale at the end of the CV. On the contrary, if the asset(s) are overvalued, the GP earns more carried interest immediately at the expense of a lower carried interest in the future.

CVs transaction feature mechanisms are aimed at reducing incentive misalignment. The most important one is certainly the rollover of the GP’s equity and the reinvestment of a large part of the carried interest. This is optimal because, by doing so, the GP puts its own capital at risk and, in other words, has “skin in the game”, which ensures it is genuinely committed to the transaction and is not using the continuation fund opportunistically. In addition to that, to balance the new risk-return profile connected to the operation, the economic terms in favour of the GP are generally weakened. For instance, as we have already mentioned, the management fee may be lowered, the hurdle rate raised, and the overall provisions made stricter. Lastly, to ensure the most impartial valuation possible, despite the mentioned pitfalls, an independent advisor is appointed to assess the value of the asset(s).

WHAT IS THE IMPACT ON RETURNS?

Early results point in a positive direction when comparing CVs to traditional buyout funds. Morgan Stanley analysed continuation vehicles across vintages from 2018 to 2023 and found a median multiple on invested capital of 1.4x, against 1.3x for buyout funds from the same period (Morgan Stanley Private Capital Advisory, 2025). An Evercore and HEC Paris study covering 297 continuation funds across the same period found that, on average, every dollar invested grew to $1.56 in total value, with single-asset vehicles outperforming multi-asset ones (Evercore and HEC Paris, 2025). The risk profile tells an equally important story. Returns for continuation funds cluster more tightly around the median with fewer extreme outcomes, demonstrated by the Gini coefficient of 0.32 versus 0.46 for buyout funds (HEC Paris, 2024, HarbourVest, 2025). Single-asset vehicles offer higher potential multiples but tie liquidity to one exit event, while multi-asset vehicles tend to return cash earlier as individual companies are sold.

RECENT TRANSACTIONS

Recent transactions illustrate this dynamic. Several large buyout firms have used continuation vehicles to retain control of flagship assets in sectors such as technology, healthcare, and business services, where growth trajectories extend beyond the original investment horizon. A notable example is the recent $1.2 billion private credit continuation vehicle led by Ares Management in partnership with Antares Capital. The transaction involved the transfer of over 100 underlying first lien, floating rate loans from existing funds into a new vehicle, providing liquidity to existing investors while allowing new investors to gain exposure to a diversified pool of high-quality credit assets.

This deal is particularly significant as it highlights two broader trends within the market. First, it demonstrates the increasing scale of continuation vehicles, with transactions now regularly exceeding the billion-dollar mark. Second, it reflects the expansion of continuation structures beyond traditional private equity into private credit, where longer asset durations and delayed exits have made liquidity solutions even more critical. The fact that this was one of Ares’ largest credit secondary investments to date further underlines the growing institutionalisation of the space and the depth of capital now available to support these transactions.

Overall, the increasing use of continuation vehicles reflects a more flexible and sophisticated private equity ecosystem. They bridge the gap between liquidity needs and long term value creation, while the shift towards single asset structures highlights a growing emphasis on quality, transparency, and alignment across all participants in the transaction.

BIBLIOGRAPHY

Duke University – The rise of private equity continuation funds

University of Chicago Booth School of Business – The rise of private equity continuation funds

https://www.chicagobooth.edu/research/stigler/research/-/media/5d46328c68e0466b9787f42d98275f3b.ashx

EGCI – The rise of private equity continuation funds

https://www.ecgi.global/system/files/2024-04/the-rise-of-private-equity-continuation-funds.pdf

Ardizzon, L. (2026). Private equity continuation vehicles. Final dissertation, Bocconi University, Bachelor in International Economics and Finance (BIEF).

Bain and Company – Global Private Equity Report 2025

Jefferies Private Capital Advisory – H1 2025 Global Secondary Market Review

Jefferies Private Capital Advisory – 2025 Global Secondary Market Review

Morgan Stanley Private Capital Advisory – The Case for Continuation Funds: An Updated Review of Initial Performance (March 2025)

https://www.secondariesinvestor.com/continuation-fund-performance-begins-to-solidify-morgan-stanley

Evercore and HEC Paris – Continuation Fund Performance Study 2025

https://en.paperjam.lu/article/continuation-funds-high-returns-low-dispersion

HarbourVest Partners – Research Validates Growing Adoption of Continuation Transactions

Campbell Lutyens – 1H 2025 Secondary Market Overview Report (August 2025)

S&P Global – Private Equity Exits Fall to 2-Year Low in Q1 2025

Antares Capital (2025). Antares Closes $1.2 Billion Private Credit Continuation Vehicle Led by Ares Management.

Lazard (2026). Secondary Market Report 2025. Lazard Private Capital Advisory

https://www.lazard.com/research-insights/lazard-2025-secondary-market-report

Comments are closed.