Written by Allegra Berni, Julius Buse, Yonatan Elkanati and Amedeo Baboin | Editor: Letizia Ianniciello

THEMATIC OVERVIEW

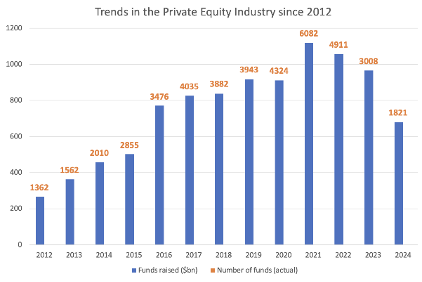

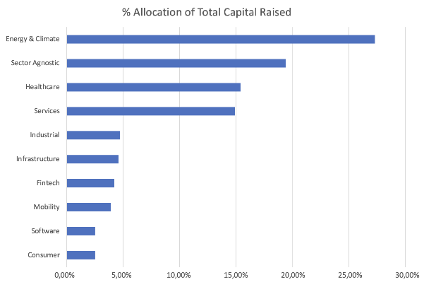

In recent years, the Private Equity industry has entered a phase of profound disruption. On the one hand, fundraising has dropped to its lowest level since 2016, largely due to a weak exit environment that constrains liquidity for limited partners and reduces their ability to commit new capital. On the other hand, the number of fund closings has fallen considerably, highlighting how especially smaller or less established general partners are struggling to attract new capital. In conjunction, investment and exit value have sharply declined since their peaks in 2021, with exit values lying beneath investment values, implying exit pressure and weak investor sentiment. Investor focus has also shifted towards the energy and utilities industry and more sector-agnostic approaches – with a very strong concentration of capital allocation to US funds (83.5%).

Source: Capvisory (2025)

As discussed, consolidation among PE firms is intensifying. Alternative asset managers have already been acquiring or merging with smaller industry peers to achieve greater scale, consolidate fundraising and deal execution and meet investors’ preferences for investments in more mature companies with stronger track records. Additionally, this trend is fuelled by heightened regulatory and compliance hurdles, stronger competition for high-quality assets, and investor preferences shifting towards lower risk asset allocation due to higher macroeconomic uncertainty.

Interestingly, the operating model of Private Equity investors is also being disrupted: KKR’s partner Alisa Wood has publicly highlighted that market volatility and liquidity constraints require GPs to focus more on returning capital to LPs and to improve operational flexibility. Accordingly, industry participants are increasingly deploying artificial intelligence to reduce rising operational costs by automating repetitive work streams and accelerating due diligence and portfolio-monitoring workflows involving deal sourcing, data extraction and predictive portfolio analytics.

Collectively, these trends of weakened liquidity, consolidation among GPs and operational cost reductions via AI are reshaping the Private Equity sector. Smaller and mid-sized funds are increasingly at risk of termination or being acquired by larger platforms – as they face higher challenges to raise capital, deliver promised exit returns and are pushed to invest into slimmer operational models, too. Therefore, consolidation and fund terminations to accelerate is expected in the coming years, reshuffling the sector’s competitive landscape.

WHY CONSOLIDATION IS EXPECTED

After two decades of rapid growth, the Private Equity sector is shifting from expansion to consolidation – as capital and activity converge around fewer, larger players. This consolidation is occurring at two levels. On one side, institutional consolidation is visible as GPs merge with smaller rivals, concentrating capital in fewer firms. On the other, portfolio consolidation intensifies through the growing prominence of buy-and-build strategies, which integrate investments into larger platforms. Together, these mechanisms are reshaping Private Equity at both the level of capital managers and the companies that receive it.

The main driver of consolidation is the tightening of fundraising conditions. Despite a rebound of deal and exit values in 2024 (up 37% and 34% respectively), global private-equity fundraising fell by 23%, according to Bain & Company’s Global Private Equity Report 2025. As less capital circulates, limited partners concentrate commitments in fewer firms. This slowdown stems from a liquidity squeeze among investors, with distributions as a share of Net Asset Value ratio plummeting to 11% — the lowest in over a decade, ranging from 25–30%. The report highlights that capital is likely to continue to consolidate in the hands of top performers and scale funds, while smaller firms will struggle to secure commitments for continuation vehicles. This mechanism creates a feedback loop: with fewer fundraising rounds, LPs reinvest in the same firms and mid-sized managers lose visibility. The effect is structural: a fundamental reshaping of the industry.

Beyond fundraising, scale has major influence. Larger firms have the capacity to absorb rising regulatory, operational and technological costs that impact smaller competitors. Scale also significantly enhances fundraising potential, as larger platforms offer investors credibility and greater diversification. Finally, it also broadens deal-sourcing reach, thus enabling participation in complex transactions that smaller firms cannot pursue.

Overall, these motivations incentivise managers to grow through M&A rather than individual expansion. According to PwC’s Equity Trend Report 2025, 64% of executives identify market consolidation as the strategy that increases equity value the most, while buy-and-build ranks second (62%). Both are correlated: as M&A among GPs accelerates and buy-and-build deals integrate smaller companies into larger platforms, concentration deepens. Sagard’s acquisition of Swiss asset manager Unigestion’s Private Equity business – described in Private Equity International – illustrates this trend. Expected to close in early 2026, the deal will consolidate Unigestion’s $12.5 billion AUM under Sagard PrivateEquity Solutions. Accordingly, Sagard’s managed assets will reach $44 billion, overseeing more than eleven strategies across its combined platform.

TREND ANALYSIS

Causes

The pressures reshaping PE are starting to show up clearly in the numbers. Performance has softened, cash is tight, and investors are becoming more selective. Recent fund vintages have missed expectations. Higher borrowing costs combined with weaker exit multiples have eaten into returns, and valuations have remained flat. Median buyout internal rates of return decreased from around 18% in 2021 to 11% in 2024. Furthermore, the so-called denominator effect has amplified the pressure: as public markets declined, many LPs found themselves overallocated to PE, forcing them to scale back new commitments. On the other hand, smaller firms – which depend on steady distributions to attract new capital – felt the impact most sharply.

A tougher exit market has made matters worse. Global fundraising fell to its lowest level since 2016, reflecting LP liquidity strain. With IPOs and secondary buyouts slowing, roughly $1tn in NAV remains tied up in ageing portfolios. Moreover, LPs are struggling to recycle capital, thus limiting commitments to newer managers. Large institutions are increasingly concentrating allocations with established and reliable platforms offering scale, transparency and technological sophistication.

Consolidation of mid-tier firms

Consolidation has accelerated among mid-sized funds, exemplified by Bridgepoint’s merger with Energy Capital Partners and Ardian’s minority European GPs. Moreover, secondary transactions have become more common – with firms selling partial ownership to larger peers, sovereign wealth funds and institutional investors – seeking stable exposure to management fees. While others, unable to raise successor funds, have wound down operations – evidence of a shrinking middle ground.

Rise of mega-fund managers

The largest firms, by contrast, are expanding. More than half of the world’s Private Equity assets are currently held by the top 25 firms. To increase their investor base and to smooth returns, groups such as Blackstone, KKR and Apollo have ventured deeper into credit, infrastructure and private wealth. Their size solidifies their dominance by providing them with the paramount financial and technological resources to create systems that their smaller industry peers cannot match.

Shift toward diversified platforms

This concentration has encouraged multi-asset platforms that combine Private Equity, credit, real estate and infrastructure. Investors favour the simplicity of a single access point. For the biggest players, diversification is both a buffer against volatility and a route to long-term growth.

Overall, Private Equity is moving towards a barbell structure, with a handful of global groups at one end and specialised boutiques at the other. Mid-tier firms are being squeezed, and many face an increasingly uncertain future.

FUTURE IMPLICATIONS

New Operating Models

Private Equity firms face a liquidity crunch from high interest rates, market volatility and weak IPO activity, significantly reducing exits. To restore liquidity, many use continuation funds – vehicles transferring portfolio companies from existing funds into new ones –financed through rolling LPs and new investors, allowing firmsto retain strong assets while giving exiting LPs a cash-out option.

In 2024, continuation funds comprised 14% of total PE exits, growing 12.9% year-on-year and outpacing the secondary market’s 8%. Almost $1 trillion USD in NAV remains tied up in ageing portfolios with negative cash flows. These models offer more flexibility than the classical ten-year model, helping managers tackle capital lockups and prolonged holding periods amidst high interest rates, weak IPOs and poor buyer appetite.

Amidst uncertainty, transparency and valuation scrutiny become critical. KKR CFO, Robert Lewin, predicts GPs to shrink, while Apollo’s Jim Zelter warns some funds “don’t realise their most recent fund is their last”. Likely winners will be mega-managers with diversified platforms and specialist boutiques. Evergreen, hybrid, and permanent-capital vehicles are also gaining traction as firms seek resilience against liquidity shocks.

Emerging Investment Strategies

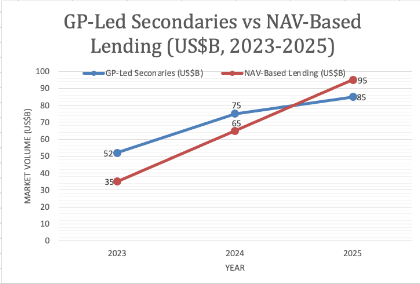

Slowing exits drive managers to diversify beyond buyouts. GP-led secondaries – GPs transfer portfolio assets to new vehicles for LP liquidity – and NAV-based lending – credit secured against a fund’s NAV – are increasingly used to unlock capital and extend fund life. Private credit continues expanding as institutions seek stable yields. Club deals and co-investments attract LPSs with greater alignment and lower fees, thematic strategies in climate infrastructure and digital transformation replace generalist mandates.

Source: Jefferies (2025); Upwelling Capital (2024); KBRA (2024)

Tech Integration

Technology is central to value creation. Firms deploy AI and predictive analytics across sourcing, diligence, and portfolio monitoring to create data-driven, proactive decisions. Many are establishing AI centres and ‘quantitative PE’ teams which merge machine learning and traditional investment analytics to model risk and optimise value. Digital dashboards and ESG analytics enhance transparency and investor confidence.

Emerging markets growth

With dealmaking slowing in developed economies, attention is shifting to regions with accelerated growth and less competition. Southeast Asia benefits from digitalisation and an increasing middle class; Africa from infrastructure gaps; and Latin America from fintech and energy transition opportunities. Institutions such as Yale and Harvard are investing in such regions via secondaries, while limited local financing creates ideal opportunities for private credit and infrastructure funds.

Bibliography

Acuris Group. (2024). Private equity fundraising: Key trends and market survey 2024. Acuris.

Retrieved from https://cdn.lawreportgroup.com/acuris/files/private-equity-law-report/documents/PW%202024%20PE%20Fundraising%20Survey.pdf

Bain & Company. (03/03/2025). Field notes from the generative AI insurgency in Private Equity.

Retrieved from https://www.bain.com/insights/field-notes-from-generative-ai-insurgency-global-private-equity-report-2025/

Bain & Company. (03/03/2025). Private Equity Outlook 2025: Is a Recovery Starting to Take Shape?

Retrieved from https://www.bain.com/insights/outlook-is-a-recovery-starting-to-take-shape-global-private-equity-report-2025/

Bloomberg. (11/09/2024). KKR’s Alisa Wood: Capital markets are normalizing [Video]. Bloomberg.

Retrieved from https://www.bloomberg.com/news/videos/2024-09-11/kkr-s-alisa-wood-capital-markets-are-normalizing-video

Capvisory. (18/02/2025). Current trends in private equity fundraising (2025).

Retrieved from https://capvisory.de/current-trends-in-private-equity-fundraising/

Ernst & Young (EY). (19/02/2024). Big gets bigger: How consolidation is reshaping Private Equity.

Retrieved from https://www.ey.com/en_lu/insights/private-equity/big-gets-bigger-how-consolidation-is-reshaping-private-equity

Infosys. (2025). Creating value with AI: Private equity. Infosys Insights.

Retrieved from https://www.infosys.com/industries/private-equity/insights/documents/creating-value-with-ai.pdf

Moonfare. (26/11/2024). Private equity is consolidating: What’s the good and the bad? Moonfare Blog.

Retrieved from https://www.moonfare.com/blog/private-equity-consolidation

S&P Global Market Intelligence. (16/01/2025). Global Private Equity fundraising sinks for 3rd straight year.

Retrieved from https://www.spglobal.com/market-intelligence/en/news-insights/articles/2025/1/global-private-equity-fundraising-sinks-for-3rd-straight-year-87110906

Comments are closed.