Written by Nour Khoury, Diletta Bolzoni, Carlo dell’Orefice and Ellen Rehn | Editor: Maciej Skorupka

The traditional and well-understood private equity model is giving way to a different model, forced by the difficult economic conditions General Partners are facing nowadays.

Historically, GPs have relied on a stated lifecycle: acquire a platform company, drive margin expansion or organic growth, and then exit via. However, elevated interest rates and the following increase in the cost of leverage have made this solution quite problematic. On top of that, subdued IPO markets and risk-averse strategic acquirers mean that assets are remaining in funds longer than anticipated.

The consequence of that is a structural mismatch between the lifespan of closed-ended funds and the maturity of portfolio companies, which leads to the problem of finding a solution of that. In the last years of the fund, the expectation is that most assets should be realised (by selling or listing them) so that Limited Partners receive distributions and the fund winds up.

However, with fewer exit opportunities and assets held longer, many firms are stuck with “legacy” companies that have matured beyond the original plan but still require time, capital or favourable market conditions to exit.

This “deadline” pressure leaves GPs in a bind: holding too long but reaching satisfying results, or disappointing LPs? The result of this approach is an era of extended holding periods, delayed realisations and escalating tension between asset lifecycles and fund structures.

Continuation Vehicles (CVs): Buying Time

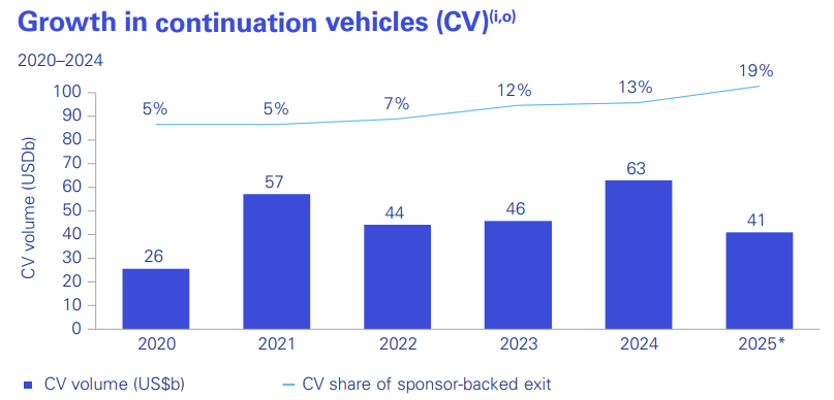

In order to face this huge problem, the industry has responded with the rise of so-called continuation vehicles (CVs) or continuation funds, new vehicles created by the same GPs to acquire one or more assets from an existing fund nearing its end-of-term. The legacy fund’s LPs are given the option to realise liquidity or roll over into the continuation structure, fresh capital is injected by new investors into what is effectively an extension of the underlying company’s holding period. Born as a niche solution to difficult existing solutions, CVs are now becoming the norm.

The idea of CVs makes sense, as they are created in order to gain extra runway to drive value creation in companies that still have upside but might not exit within the original fund term. For LPs in particular, those wishing to realise earlier, CV²s offer liquidity when the broader market is unwilling or unable to transact.

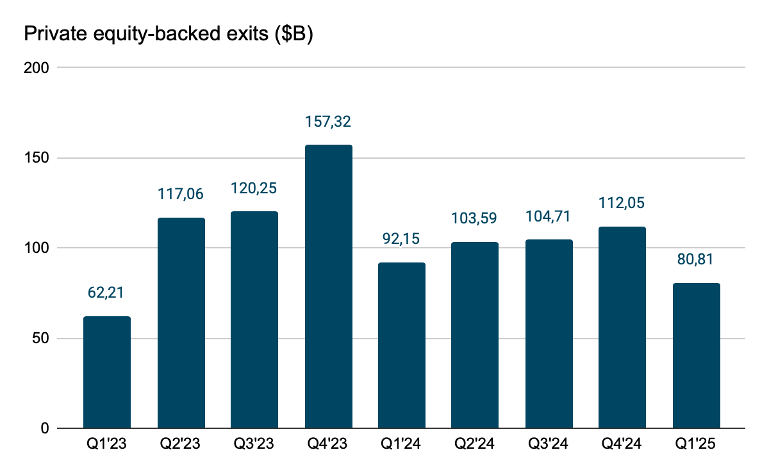

However, while CVs provide a clever workaround to the “deadline problem,” they are not without complexities. Many GPs believe their portfolio companies still have meaningful upside, especially in today’s market, where exit conditions remain challenging, and it is often more profitable to hold them a bit longer before selling. According to an S&P Global Market Intelligence Analysis, global private equity exit activity fell to a two-year low in early 2025, with only 473 exits worth $80.81 billion in the first quarter of 2025, which both represent the lowest figures since the first quarter of 2023.

Selling now might mean accepting lower valuations, yet holding on within the original fund is often no longer possible as it nears its legal term. This tension is at the heart of the CV dynamic: existing LPs want to sell their stakes at the highest possible price, while new investors want to buy in at the lowest valuation. As both seller and buyer in the transaction, the GP faces an inherent conflict of interest: setting too low a valuation disadvantages existing LPs, while setting it too high undermines the credibility and return potential of the new fund. To ensure these transactions are fair, investors increasingly demand third-party valuations and independent fairness opinions.

“CV²s” Funds: Rolling the Rollovers

As CVs mature, the same challenge reappears: many assets still aren’t ready for a clean exit. To address this, GPs are creating “CV²s” – new continuation vehicles that buy assets from the original CV and extend the holding period. The aim is to hold high-quality companies through a difficult exit environment, give managers more time to grow them, and sell later at better valuations once markets and financing conditions recover. In markets constrained by high rates and limited exit options, this has become a common way to preserve value today and capture more of it tomorrow.

CV²s also respond to sponsors’ need for liquidity. By rolling assets from one vehicle to the next, managers can offer liquidity to existing investors while retaining ownership of high-performing, long-dated assets. This continuous capital-recycling loop turns illiquid holdings into a semi-liquid, renewable capital engine and moves PE away from the traditional ‘buy-improve-sell’ cycle toward a model where assets circulate within the same ecosystem of funds.

Why Investors Accept It (For Now)

So far, investors are accepting – and in many cases embracing – this model. CVs have modestly outperformed traditional funds, posting median multiples of 1.4× versus 1.3×, largely due to better-known assets, faster deployment, and lower entry valuations. In addition, they offer a more flexible structure which allows for deeper customisation and greater control. Yet as the model scales, conflicts of interest have become harder to ignore. Existing LPs naturally seek the highest possible exit price, while new LPs prefer the lowest possible entry point – putting GPs in a bind. In one case, they’re incentivised to underprice assets to make the new CV’s returns look stronger; in the other, to overprice them to avoid marking losses in the old fund. This tension has led LPs to demand greater transparency, independent valuations, and third-party fairness opinions to ensure these engineered rollovers remain credible and aligned with fiduciary standards.

Structural Shift and Main Risks

Repeated rollovers make it easier, psychologically and politically, to hold on to assets when an exit would crystallise disappointing returns, and the depth of the secondary market reinforces this. According to the Financial Times, secondaries reached a record $162bn in 2024, normalising the use of CVs and CV²s as internal liquidity routes when external buyers are scarce.

The risk is that this becomes a quiet form of evergreening: assets are moved into new vehicles, delaying valuation tests by external buyers. As funds age, reported Net Asset Values (NAVs) hold up or rise while distributions to LPs fall. This “zombie” dynamic creates a liquidity problem first and a confidence problem next, making it harder to distinguish genuine operating progress from simple duration management.

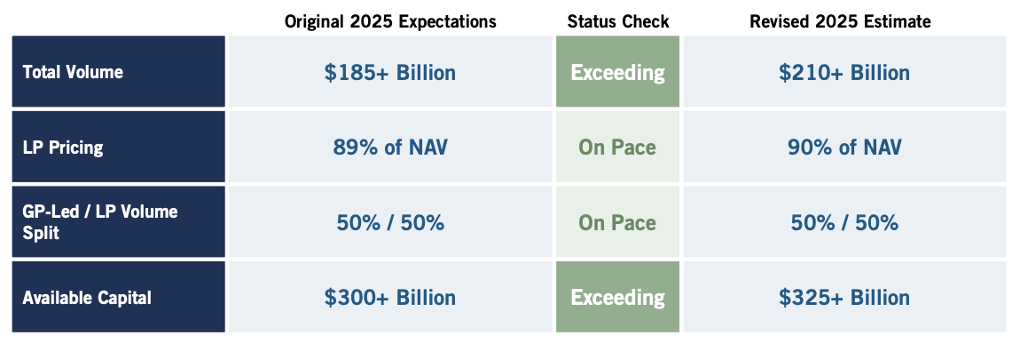

Thus, scale is what makes CVs and CV²s feel routine: volumes are large enough to absorb inventory, a great part of the flow sits where CVs live, and pricing near book implies that rolling forward often looks preferable to selling at a discount. On this matter, Jefferies Semi-Annual Secondary Market Review reports $103bn of volume in H1 2025, of which $47bn is GP-led, with the average pricing for LP portfolios at 90% of NAV.

Summary

The traditional private equity model is going through a structural transformation mainly due to high interest rates, slow-moving IPO markets, and limited exit opportunities. In order to manage this, PE firms created continuation vehicles (CVs) – new funds to acquire ageing assets from expiring ones, and at the same time offering liquidity to existing investors and more time for value creation. As first-generation CVs mature, “CV²s” funds are introduced. They are tools to further extend ownership and effectively recycle capital within the same ecosystem. While these mechanisms provide flexibility and preserve asset value, they are also exposed to some risks, including evergreening-like dynamics and conflicts of interest. Looking ahead, the private equity landscape is likely to evolve toward a more continuous model of capital management, one that puts liquidity engineering and long-term involvement over the traditional buy-improve-sell cycle.

Bibliography

Private Equity Faces Pockets of Distress for Long-Held Assets;https://www.bloomberg.com/news/articles/2025-01-16/private-equity-faces-pockets-of-distress-for-long-held-assets

L’opportunità dei co-investimenti (The Case for Co Investments);https://www.gsam.com/content/dam/gsam/pdfs/international/it/articles/the-case-for-co-investments-it.pdf?sa=n&rd=n

Investors Offloaded Record Volume of Private Equity Stakes in 2024; https://www.ft.com/content/e8bbc1b8-93fb-4f0f-9c95-65341c299f30

H1 2025 Global Secondary Market Review; https://www.jefferies.com/wp-content/uploads/sites/4/2025/08/Jefferies-Global-Secondary-Market-Review-July-2025.pdf

Night of the Living Fund: The Rise of Zombie Private Equity; https://www.msci.com/research-and-insights/blog-post/night-of-the-living-fund-the-rise-of-zombie-private-equity

Private Equity Exits Fall to 2-Year Low in Q1 2025; https://www.spglobal.com/market-intelligence/en/news-insights/articles/2025/4/private-equity-exits-fall-to-2year-low-in-q1-2025-88524467?utm_source=chatgpt.com

Private Equity Exits Pacing for 5-Year Low After Slow H1; https://www.spglobal.com/market-intelligence/en/news-insights/articles/2024/7/private-equity-exits-pacing-for-5-year-low-after-slow-h1-82435868

Value Creation in Private Equity; https://kpmg.com/xx/en/our-insights/value-creation/value-creation-in-private-equity.html

Comments are closed.