Written by Antonio Alessandro Livraghi, Gideon Ots and Michelangelo Parlato

Growth equity as a resilient strategy amid volatility

Growth equity, situated between venture capital and traditional buyouts, focuses on acquiring minority stakes in established, high-growth companies that are beyond the startup phase but not yet suited for buyout funding. Investment targets are usually middle-market firms with proven business models, strong organic growth, and a clear path to profitability – often in sectors like software, healthcare, or business services.

Post-pandemic, Europe’s economic landscape has been marked by persistent inflation, rising interest rates, and geopolitical tensions. These factors have contributed to valuation adjustments across various sectors. Amidst this volatility, growth equity has demonstrated resilience within European private markets.

This article explores how growth equity is positioned within the broader European PE landscape, and why it continues to gain strategic relevance for investors in today’s complex macro environment.

Positioning growth equity within private markets

Growth equity is often misunderstood as a “middle ground” between venture capital and buyouts, but it has clearly defined characteristics that differentiate it from both. Unlike venture capital, which targets pre-revenue or early-revenue startups, growth equity investors seek companies with validated business models, positive cash flow, and identifiable paths to profitability. These firms typically operate in expanding markets but require external capital to seize strategic inflection points.

In contrast to buyouts, growth equity does not rely on high leverage or full control. Investors usually take minority stakes and act as strategic partners rather than operators, helping scale the business through value-creation initiatives such as talent acquisition, digital transformation, or international market entry. The absence of heavy debt also mitigates interest rate risk. This positioning – less risky than VC, less levered than buyouts – has made growth equity particularly attractive to LPs navigating uncertain economic conditions.

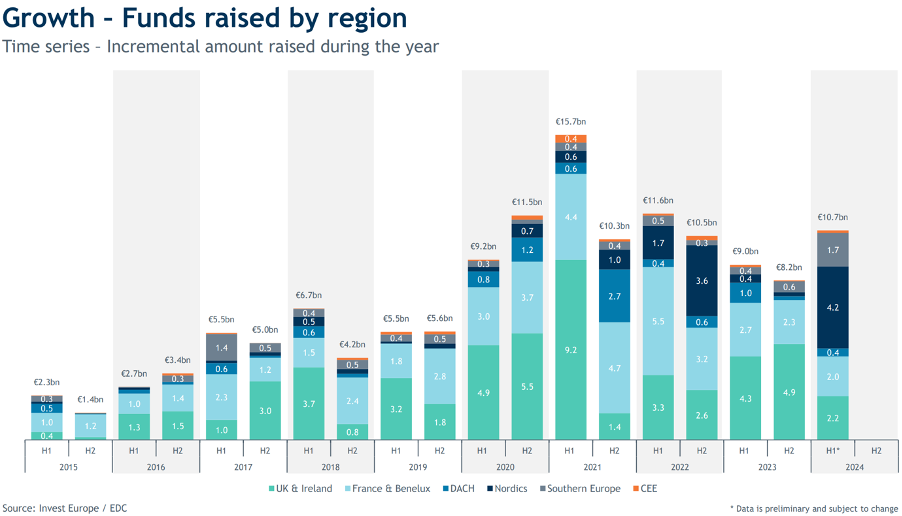

In Europe, the growth equity landscape has expanded significantly. Between 2018 and the first half of 2021, the number of growth equity deals increased from 1,200 to nearly 1,600, indicating robust investor interest and a strong pipeline of opportunities. Over the past five years, more than $100 bn has been raised with mandates to invest in European companies in the growth equity stage. In the first half of 2024, growth funds raised €10.7 bn, marking a 20% increase from the same period in 2023 and returning to levels observed in late 2022.

Where Capital Meets Momentum: Technology and Healthcare in Focus

This strategic positioning makes growth equity particularly well suited to supporting high-growth companies in technology & software and healthcare & life sciences, which together account for over 80% of Europe’s current growth-stage deal flow. Companies in sectors like biopharma, fintech, and payment solutions have emerged as pivotal candidates transitioning from venture-backed stages into growth equity investment. A more selective, and often more challenging, approach targets mature verticals, where VC investment is declining but growth equity offers opportunities for strategic investors.

The technology and software sector possesses key characteristics that make it an ideal target for growth equity investments. Companies in this space, especially Software as a Service (SaaS) providers, benefit from scalable business models, allowing them to expand operations with minimal marginal costs. Their subscription-based revenue structures offer predictable and recurring income, enhancing investor appeal. Whether it is deep tech firms specializing in AI or cybersecurity and creating entirely new markets, or more traditional businesses undergoing digital transformation, the sector continues to offer compelling opportunities for long-term value creation.

ReliaQuest, a Tampa-based cybersecurity firm specializing in AI-powered threat detection and response automation, secured over $500 million in a growth funding round in Q1 2025. The round was led by EQT Growth, with participation from KKR and FTV Capital, and brought the company’s valuation to $3.4 billion. ReliaQuest exemplifies the key characteristics that make a company ideal for this type of funding: profitable, scaling rapidly, and demonstrating momentum with over $300 million in annual recurring revenue and a 30% YoY growth.

The Healthcare sector offers compelling opportunities for growth equity, yet presents unique challenges. Life sciences businesses, especially those serving pharmaceutical and biotech firms, are defined by high switching costs, strict regulatory frameworks and significant barriers to entry. These contribute to predictable revenue streams, strong customer retention and attractive margins, creating an ideal environment for growth equity investors seeking low-risk opportunities. In healthcare services, value creation is possible by shifting care delivery from costly hospital settings towards more scalable and efficient alternatives like clinics and physician groups. However, many healthcare companies are founder-led, often by clinicians with limited exposure to finance. Therefore, it is essential for growth equity investors to align incentives, strategy and expectations early on, fostering a shared vision and value-driven partnership.

In early 2025, Navina, a growth-stage company operating in the health IT segment (one of the most resilient in the health-tech landscape), raised $55 million in a Series C round led by Goldman Sachs Alternatives Growth Equity, bringing its total funding to $100 million. Navina’s AI copilot supports over 10,000 clinicians across 1,300 clinics, delivering proactive clinical intelligence at every outpatient interaction, which reduces physician burden and improves patient outcomes.

Regional Dynamics in European Growth Equity: From Mature Hubs to Emerging Markets

European growth equity activity in 2024 has been led by the continent’s strongest economies, with notable shifts among regions. Western Europe remains dominant, especially France & Benelux and the UK & Ireland. In 2023, companies in France & Benelux attracted the most growth funding at about €7.8 billion, slightly surpassing the UK–Ireland region. The UK still boasts Europe’s deepest investor base – London remains a hub for large growth equity managers and accounted for the largest fundraising in H1 2024 (over €20 billion in UK/Ireland). DACH (Germany, Austria, Switzerland) and the Nordics also contribute significantly; industry surveys anticipated the strongest deal growth in 2024 to come from DACH, followed by France and the Nordics. These Western European hubs benefit from mature ecosystems and a steady flow of tech scale-ups seeking growth capital.

Southern Europe and Benelux countries are emerging as vibrant growth equity areas as well. Paris and Amsterdam now rank among Europe’s top regions for investment activity, reflecting a varied dispersion of growth deals. In contrast, Central and Eastern Europe’s (CEE) share of European PE investment is still small (only ~3% of total value in 2021) , underscoring the gap with Western markets. Nonetheless, CEE is gaining momentum with rising deal flow in hubs like Poland and the Baltics, supported by strong economic growth and increasing interest from pan-European General Partners (GPs) . Western Europe’s growth equity market is highly developed (0.8% of GDP invested vs just 0.2% in CEE), whereas Eastern regions are building capacity and investor networks. This creates notable differences: Western Europe sees larger deal sizes and more competition, while CEE offers greenfield opportunities but relies more on development institutions and cross-border investors.

Outlook: Navigating Growth Amid Recovery and Realignment

As of late 2024 and into early 2025, the outlook for European growth equity is cautiously optimistic. Tech remains the fuel of growth investing whilst IT/software sector had its best deal value year since 2021, with investors continuing to favour high-growth tech, digital, and healthcare companies. Notably, GPs are also observing emerging areas like artificial intelligence and deep tech; 68% of European fund managers say AI-related investments are becoming more attractive than before In addition, sustainable energy and infrastructure have seen substantial activity, pointing to increased capital flowing into clean-tech themes.

Macroeconomic conditions are central in shaping fund strategies. After a period of high inflation and interest rate hikes, Europe’s financial outlook is improving. Inflation has stabilized and central banks began easing – the ECB and others cut rates multiple times in the second half of 2024. Narrowing valuation gaps between buyers and sellers are making it easier to strike deals. Meanwhile, PE firms are armed with near-record dry powder, pressuring GPs to deploy capital. All these factors support a pickup in growth deal activity going into 2025. However, many companies remain in wait-and-see mode, especially in light of ongoing macroeconomic uncertainty dominating the global landscape.

Exit markets remain a mixed picture: The IPO window in Europe has been sluggish – 2024 saw a few high-profile listings (e.g. CVC Capital Partners’ own IPO), but by Q3 only two small IPOs occurred and many of the year’s listings were trading below their offering price. As a result, exit values for European PE were flat versus 2023 and still over 30% below the 2021 peak .

European growth equity has proven its resilience in a challenging macro environment, offering a differentiated investment alternative between venture capital and buyouts by backing scalable, high-growth companies with proven models. Technology and healthcare sectors continue to anchor deal flow, driven by strong fundamentals, recurring revenues, and long-term transformation trends. Regionally, while mature markets in Western Europe continue to dominate capital flows, other regions are emerging as new hubs of opportunity. Looking ahead, the outlook for 2025 is cautiously optimistic: easing inflation, lower interest rates, and abundant dry powder suggest a potential rebound in transactions, yet global uncertainty, including the effects of new tariff policies, may lead many companies to adopt a more cautious stance. Still, with sectoral momentum and strategic capital, growth equity is well positioned to play a central role in Europe’s PE landscape in the years to come.

BibliographyInvest Europe, INVESTING IN EUROPE: PE ACTIVITY IN H1 2024, https://www.investeurope.eu/media/b4eha4ke/20241108_invest-europe_h1-activity_2024.pdfMoonfare, Growth Equity: Staying Private for Longer, https://www.moonfare.com/white-papers/growth-equity-staying-private-for-longerMcKinsey, Global Private Markets Report 2025: PE emerging from the fog. https://www.mckins/industries/private-capital/our-insights/global-private-markets-repor

CFI, Growth Equity, https://corporatefinanceinstitute.com/resources/valuation/growth-equity/?utm

BCG, Europe’s Growth Equity Landscape, https://www.bcg.com/publications/2024/opportunity-in-europes-growth-equity-landscape?utm

Dealroom & MTIP Report (2024) – “Growth Equity in European Healthtech”

https://dealroom.co/reports/growth-equity-in-european-healthtech-2024

Global Private Markets Report 2025: PE emerging from the fog https://www.mckins/industries/private-capital/our-insights/global-private-markets-report

European PE Outlook 2024: Positive momentum in the air

Comments are closed.