By Edoardo Libero Ruffo and Tommaso Alocci

The Public Exchange Offer (OPS) by MPS

On January 24, 2025, Monte dei Paschi di Siena (MPS) announced a Public Exchange Offer (OPS) for Mediobanca, one of Italy’s leading financial institutions. The operation, with a total value of

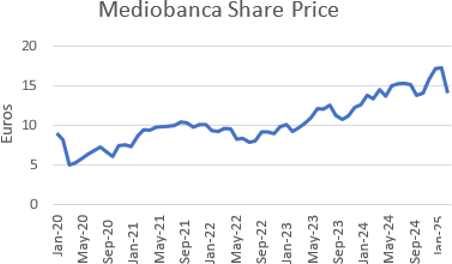

€13.3 billion, aims at acquiring 100% of Mediobanca’s share capital, with the goal of creating a major national banking group. The proposal includes a share swap: for each Mediobanca share, MPS offers 2.3 new MPS shares. Based on MPS’s closing price on January 23, 2025 (€6.953), this values each Mediobanca share at €15.99, representing a 5% premium over its market price of €15.23 (share price at the time of the takeover).

What is an OPA?

An Offerta Pubblica di Acquisto (OPA), or Takeover Bid, is a public offer through which a company or investor proposes to acquire shares of a listed company at a set price – typically above market value – with the aim of taking control or increasing its stake. OPAs can be voluntary, launched at the discretion of the bidder, or mandatory, triggered by legal thresholds (such as surpassing 30% ownership). Some OPAs are full (seeking 100% of the shares), while others are partial. When the consideration is paid in shares rather than cash, the operation is referred to as a Public Exchange Offer (OPS), as is the case with MPS’s bid for Mediobanca.

Monte dei Paschi di Siena

Founded in 1472, Monte dei Paschi di Siena is the world’s oldest operating bank. Headquartered in Siena, it has historically been rooted in Tuscany. After a long period of crisis that led to a

government bailout in 2017, the bank gradually returned to profitability. While it concluded its restructuring phase in 2023, the Italian Ministry of Economy and Finance still owns 39.2% of the bank as of late 2024. This government presence remains a point of debate, especially given the political implications of major strategic moves. The offer for Mediobanca marks a strategic turning point for MPS: from a rescued institution to a proactive player in the consolidation of Italy’s banking sector. With this deal, MPS aims to broaden its capabilities and gain access to Mediobanca’s strengths in investment banking and wealth management.

Mediobanca

Founded in 1946 in Milan, Mediobanca is a cornerstone of Italy’s financial history. It has long been at the centre of the country’s relationship-driven finance, playing a central role in the development of many major Italian corporations. In recent years, the bank has successfully diversified its activities, particularly in wealth management (e.g., via CheBanca!) and advisory services. Today, Mediobanca is seen as a highly efficient, profitable, and well-managed institution. With its balanced business model-spanning investment banking, consumer credit, and private banking – it is both an attractive acquisition target and a fiercely defended institution by its current leadership.

MPS’s Rationale Behind the OPS

According to MPS, the proposed merger is a strategic move to create a national banking champion that can compete on the European stage. The goal is to diversify its business model by integrating MPS’s retail banking base with Mediobanca’s expertise in higher-value segments such as investment banking and wealth management. CEO Luigi Lovaglio, a veteran banking executive who previously led MPS’s restructuring, described the merger as an opportunity to build a “solid, integrated, and diversified” institution. He emphasised the potential for significant operational synergies due to the limited overlap between the two entities. Addressing investor concerns, Lovaglio stressed that “risks are minimal” and reaffirmed that the focus is on Mediobanca’s core business, not its equity holdings – specifically its stake in insurance giant Generali. The move fits a broader consolidation trend in the Italian banking system and signals MPS’s ambition to become a resilient, independent European banking group.

Mediobanca’s Response

At the Morgan Stanley European Financials Conference, Mediobanca CEO Alberto Nagel unequivocally rejected MPS’s proposal, calling it “value-destroying” and detrimental to both institutions and their shareholders. He cited a detailed internal analysis showing significant risks – particularly in terms of revenue loss in private and investment banking – that he believes cannot be offset by MPS’s “ambitious” cost savings. Nagel also dismissed expectations of funding synergies, noting that credit rating agencies placed Mediobanca under negative watch

and that the bank’s private clients require higher returns than traditional retail depositors. Moreover, in his view, the deal would result in a double-digit dilution of earnings per share (EPS) and dividends per share (DPS) for MPS shareholders. Instead, Nagel advocated for Mediobanca’s standalone path, pointing to robust organic growth, €4 billion in planned shareholder distributions, and an estimated 13% dividend yield over the next 18 months – all with low execution risk. He closed by reaffirming the bank’s commitment to independence, emphasising that decisions would be guided by economic merit rather than political pressure.

Impact on Corporate Governance

If successful, the acquisition would mark a dramatic shift in Mediobanca’s governance structure—long one of the Italian economy’s most influential financial institutions. Historically, Mediobanca has operated under a relatively stable shareholder structure, with heavyweight investors like Delfin (the Del Vecchio family’s holding company) and the Caltagirone Group holding 19.81% and 7.66% stakes, respectively. These shareholders have played a key role in shaping the bank’s strategic direction while largely respecting its independence.

An MPS takeover would upset that balance. With the Italian government still holding a stake in MPS – albeit one that has been gradually reduced – the deal would introduce a semi-public controlling entity into the mix. That alone raises questions. Political undertones continue to loom over MPS’s governance, and its control of Mediobanca would almost certainly lead to changes at the board level and in executive appointments. That, in turn, could threaten the degree of autonomy that Mediobanca has historically maintained. The knock-on effects would likely extend to its relationships with other financial players – among them Assicurazioni Generali, in which Mediobanca owns a roughly 13% stake. Its stake presents a strategic integration of financial and insurance services where key synergies make the leading players in their respective industries.

Effect on the Wider Financial Ecosystem

A deal of this magnitude wouldn’t happen in a vacuum. In the insurance space, Mediobanca’s shareholding in Generali – Europe’s third-largest insurer – would likely come under the microscope as investors and regulators try to gauge how a change in ownership might steer strategic decisions.

On the banking side, the move would add another layer of complexity to an already active consolidation landscape. Intesa Sanpaolo and UniCredit, the two largest Italian banks by market cap and total assets, are unlikely to sit this out. UniCredit has made no secret of its appetite for inorganic growth, as shown by its recent push for Commerzbank, fueled by its mission to become a leading European bank to compete with US firms. Although there is a long road ahead for UniCredit, market consolidation in the EU banking sector is a strategy supported by governing bodies (i.e. the EU) as well.

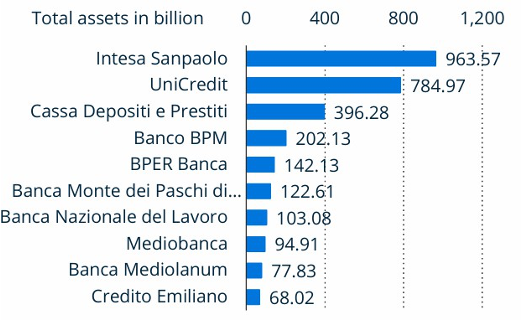

The numbers alone would be hard to ignore if the deal goes through. MPS currently ranks sixth and Mediobanca eighth by total assets; their combination would vault MPS into the number three spot nationally. That kind of shift could spark renewed interest in a sector that, for years, has been treated with caution by both private equity firms and foreign banks.

Regulatory and Market Reactions

This won’t be an easy regulatory lift. The EU has a well-established reputation for scrutinising major M&A deals – especially those with systemic implications. Antitrust, market concentration, and systemic risk would all be under the microscope. While the ECB has been a vocal supporter of banking consolidation, it’s unclear whether an MPS–Mediobanca tie-up fits the mold of a pan-European “financial champion.”

Scepticism hasn’t been in short supply. MPS’s troubled past casts a long shadow, including its state bailout, a mountain of non-performing loans, and murky derivative dealings. The government may be on board, but investors have not yet been convinced. Mediobanca CEO Alberto Nagel has publicly voiced doubts about the transaction, and the market seems to agree. Rating agencies have placed Mediobanca under negative watch, and analysts have flagged concerns ranging from integration risk to potential earnings dilution.

Then there’s the political dimension. With elections approaching and public scrutiny intensifying over the state’s role in banking, any move that appears to concentrate influence in a semi-public entity will draw fire. For now, investor sentiment leans heavily in favour of Mediobanca staying independent – a signal that confidence in its standalone strategy still outweighs enthusiasm for a state-tinged tie-up with MPS.

A Recent Twist: Golden Power Set Aside, But Questions Remain

The OPS launched by MPS for Mediobanca marks a bold bid to reshape Italy’s financial landscape. While MPS presents it as a strategic leap, concerns over integration risks, earnings dilution, and political influence remain. Mediobanca’s leadership firmly opposes the deal, and market sentiment has been cautious. In a recent development, the Italian government has decided not to exercise its golden power, signalling a non-interventionist stance despite its significant stake in MPS. Yet, political implications persist – especially with elections looming. The final outcome could redefine the balance of power within Italy’s banking system for years to come.

Bibliography

Mediobanca Shareholder Structure, https://www.mediobanca.com/en/corporate- governance/shareholders.html

Mediobanca Insurance Activities, https://www.mediobanca.com/en/insurance.html

Generali Ownership Structure, https://www.generali.com/it/investors/share-information- analysts/ownership-structure

Reuters – MPS CEO Tests Market with Mediobanca Bid,

https://www.reuters.com/markets/deals/mps-chief-puts-revamp-worlds-oldest-bank-market- test-with-mediobanca-bid-2025-04-14/

Moody’s Rating Action on Mediobanca,

https://www.mediobanca.com/static/upload_new/med/0001/mediobanca-rating_action- moodys-ratings-affirms-31jan2025-pr_501825.pdf

Reuters Breakingviews – The Generali Game, https://www.reuters.com/breakingviews/italys- great-generali-game-enters-fateful-round-2025-03-10/

Financial Times – Coverage on MPS-Mediobanca Deal, https://www.ft.com/content/76793794- 0d1a-42df-b917-52ac85535c77

Reuters – MPS: Minimal Execution Risks in Mediobanca Bid,

https://www.reuters.com/markets/deals/monte-dei-paschi-says-execution-risks-minimal- answering-iss-over-mediobanca-bid-2025-03-31/

Mediobanca Press Release – Board of Directors, https://www.mediobanca.com/static/upload_new/pre/press-release-bod-28-01-25-final.pdf

Euronext – Mediobanca Share Price, https://live.euronext.com/en/product/equities/IT0000062957-MTAA

Statista – Leading Banks in Italy by Total Assets, https://www-statista-com.lib.ezproxy.hkust.edu.hk/statistics/693548/leading-banks-assets-italy/

Comments are closed.